Een nieuwe rol voor het auditcomité en een aangepast audit rapport

|

|

|

- Frieda van de Veen

- 8 jaren geleden

- Aantal bezoeken:

Transcriptie

1 Een nieuwe rol voor het auditcomité en een aangepast audit rapport Jean-François CATS Inhoud van de uiteenzetting Nieuwe opdrachten van het auditcomité ingevoerd door de Audit Directieve en het Audit Reglement Een aangepast audit rapport : Voorstelling van Key audit matters (ISA 701) 1

2 Huidige opdrachten van het Audit Comité Financiële informaties Interne Audit Auditcomité Risicobeheer en interne controle Relaties met de commissaris Bronnen van nieuwigheden mbt Audit Comité RICHTLIJN 2014/56/EU VAN HET EUROPEES PARLEMENT EN DE RAAD VAN 16 APRIL 2014 tot wijziging van de richtlijn 2006/43/EG met betrekking tot de wettelijke controles van de jaarrekeningen en de geconsolideerde jaarrekeningen REGLEMENT (EU) No 537/2014 VAN HET EUROPEES PARLEMENT EN DE RAAD VAN 16 APRIL 2014 betreffende specifieke eisen voor de wettelijke controles van financiële overzichten van organisaties van openbaar belang en tot intrekking van het Besluit 2005/909/EG van de Commissie 2

3 Nieuwe opdrachten voor het auditcomité voorzien in het Reglement «Audit» Contrôle van de onafhankelijkheid van de commissaris Het nieuwe Europese reglement «audit» voorziet dat «Als de afhankelijkheid van een wettelijke auditor of het auditkantoor van één cliënt te groot wordt, moet het auditcomité op goede gronden beslissen of de wettelijke auditor of het auditkantoor de wettelijke controle verder mag uitvoeren. Bij het nemen van die beslissing moet het auditcomité onder meer de bedreigingen voor de onafhankelijkheid en de gevolgen van een dergelijke beslissing in overweging nemen. Nieuwe opdrachten voor het auditcomité voorzien in de Richtlijn «Audit» Relatie met de commissaris De nieuwe richtlijn «Audit» voorziet dat het Audit comité het toezichthoudende orgaan in kennis dient te stellen van het resultaat van de wettelijke controle, en toe te lichten op welke wijze de wettelijke controle heeft bijgedragen tot de integriteit van de financiële verslaglegging en welke rol het auditcomité in dat proces heeft gespeeld De verantwoordelijkheid draagt voor de procedure voor de selectie van wettelijke auditor of auditkantoor en het voordragen van de te benoemen wettelijke auditor of auditkantoor. 3

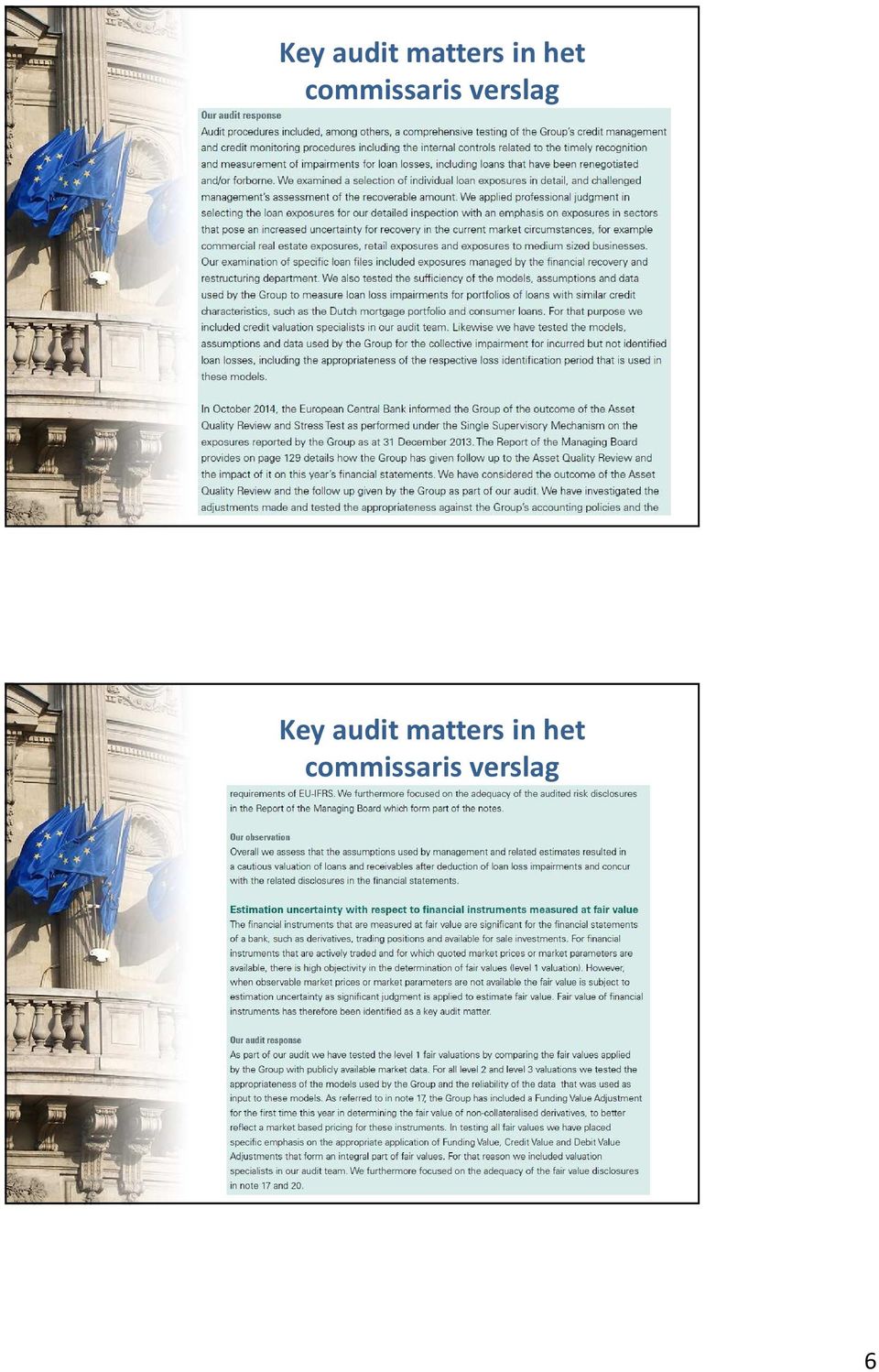

4 De «Key audit matters» worden opgenomen in het door ISA 701 De auditor vermeld in het 2de deel van het rapport de belangrijke elementen die voorgekomen zijn tijdens de audit en de wijze waarop ze opgelost werden. ISA 701 treedt in werking voor de rapporten over de afgesloten jaarrekeningen vanaf 15 december 2016 (een vervroegde toepassing is toegelaten). De Key audit matters worden opgenomen in een specifieke sectie van het rapport en worden als volgt voorgesteld : Key audit matters are those matters that, in our professional judgment, were of most significance in our audit of the financial statements of the current period. These matters were addressed in the context of our audit of the financial statements as a whole, and in forming our opinion thereon, and we do not provide a separate opinion on these matters. 4

5 De tekst van het rapport met betrekking tot de verantwoordelijkheid van de auditor zal eveneens worden melding omvatten : From the matters communicated with those charged with governance, we determine those matters that were of most significance in the audit of the financial statements of the current period and are therefore the key audit matters. We describe these matters in our auditor s report unless law or regulation precludes public disclosure about the matter or when, in extremely rare circumstances, we determine that a matter should not be communicated in our report because the adverse consequences of doing so would reasonably be expected to outweigh the public interest benefits of such communication. Voorbeeld : ABN AMRO

6 6

7 7

8 8

ISA 701, Het communiceren van kernpunten van de controle in de controleverklaring van de onafhankelijke auditor

INTERNATIONAL STANDARD ON AUDITING (ISA) ISA 701, Het communiceren van kernpunten van de controle in de controleverklaring van de onafhankelijke auditor Copyright IFAC Deze Internationale controlestandaard

INTERNATIONAL STANDARD ON AUDITING (ISA) ISA 701, Het communiceren van kernpunten van de controle in de controleverklaring van de onafhankelijke auditor Copyright IFAC Deze Internationale controlestandaard

Nieuwe en herziene Standaarden inzake de controleverklaring en wijzigingen in andere Standaarden

Originally developed by: Translated and re-published by: Royal NBA (The Royal Netherlands Institute of Chartered Accountants) Dit document maakt gebruik van bladwijzers Nieuwe en herziene Standaarden inzake

Originally developed by: Translated and re-published by: Royal NBA (The Royal Netherlands Institute of Chartered Accountants) Dit document maakt gebruik van bladwijzers Nieuwe en herziene Standaarden inzake

ISA 705 (Herzien), Aanpassingen van het oordeel in de controleverklaring van de onafhankelijke auditor

, Aanpassingen van het oordeel in de controleverklaring van de onafhankelijke auditor") INTERNATIONAL STANDARD ON AUDITING (ISA) ISA 705 (Herzien), Aanpassingen van het oordeel in de controleverklaring van de onafhankelijke auditor Copyright IFAC Deze Internationale controlestandaard (ISA)

INTERNATIONAL STANDARD ON AUDITING (ISA) ISA 705 (Herzien), Aanpassingen van het oordeel in de controleverklaring van de onafhankelijke auditor Copyright IFAC Deze Internationale controlestandaard (ISA)

Samenstelling en takenpakket van het auditcomité. Het nieuw commissarisverslag en het verslag aan het auditcomité

Samenstelling en takenpakket van het auditcomité. Het nieuw commissarisverslag en het verslag aan het auditcomité Tom MEULEMAN Vice-President IBR-IRE 1 De rol van het auditcomité 2 Evolutie Auditcomités

Samenstelling en takenpakket van het auditcomité. Het nieuw commissarisverslag en het verslag aan het auditcomité Tom MEULEMAN Vice-President IBR-IRE 1 De rol van het auditcomité 2 Evolutie Auditcomités

VERTALING NEDERLANDS INTERNATIONAL STANDARD ON AUDITING 705 INTERNATIONAL STANDARD ON AUDITING 705

INTERNATIONAL STANDARD ON AUDITING 705 INTERNATIONAL STANDARD ON AUDITING 705 MODIFICATIONS TO THE OPINION IN THE INDEPENDENT AUDITOR S REPORT AANPASSINGEN VAN HET OORDEEL IN DE CONTROLEVERKLARING VAN

INTERNATIONAL STANDARD ON AUDITING 705 INTERNATIONAL STANDARD ON AUDITING 705 MODIFICATIONS TO THE OPINION IN THE INDEPENDENT AUDITOR S REPORT AANPASSINGEN VAN HET OORDEEL IN DE CONTROLEVERKLARING VAN

Aanpassingen van het oordeel in de controle- verklaring van de onafhankelijke accountant 7 januari 2016

Originally developed by: Translated and re-published by: Royal NBA (The Royal Netherlands Institute of Chartered Accountants) Dit document maakt gebruik van bladwijzers Translated and re-published by:

Originally developed by: Translated and re-published by: Royal NBA (The Royal Netherlands Institute of Chartered Accountants) Dit document maakt gebruik van bladwijzers Translated and re-published by:

((statutaire) vestigingsplaats).

vestigingsplaats).") Nederlands Let op: dit is een voorbeeldtekst! Engels 00 Voorbeelden oob-controleverklaringen (Controlestandaarden 700-799) 0. Controleverklaringen in overeenstemming met Standaard 702N 0.1.1 Goedkeurende

Nederlands Let op: dit is een voorbeeldtekst! Engels 00 Voorbeelden oob-controleverklaringen (Controlestandaarden 700-799) 0. Controleverklaringen in overeenstemming met Standaard 702N 0.1.1 Goedkeurende

Scope of this ISA 1-2 Reikwijdte van deze ISA 1-2. Effective Date 3 Ingangsdatum 3. Objective 4 Doelstelling 4. Definitions 5 Definities 5

ISA 720 v0.1 INTERNATIONAL STANDARD ON AUDITING 720 THE AUDITOR S RESPONSIBILITIES RELATING TO OTHER INFORMATION IN DOCUMENTS CONTAINING AUDITED FINANCIAL STATEMENTS (Effective for audits of financial

ISA 720 v0.1 INTERNATIONAL STANDARD ON AUDITING 720 THE AUDITOR S RESPONSIBILITIES RELATING TO OTHER INFORMATION IN DOCUMENTS CONTAINING AUDITED FINANCIAL STATEMENTS (Effective for audits of financial

Process Mining and audit support within financial services. KPMG IT Advisory 18 June 2014

Process Mining and audit support within financial services KPMG IT Advisory 18 June 2014 Agenda INTRODUCTION APPROACH 3 CASE STUDIES LEASONS LEARNED 1 APPROACH Process Mining Approach Five step program

Process Mining and audit support within financial services KPMG IT Advisory 18 June 2014 Agenda INTRODUCTION APPROACH 3 CASE STUDIES LEASONS LEARNED 1 APPROACH Process Mining Approach Five step program

Building the next economy met Blockchain en real estate. Lelystad Airport, 2 november 2017 BT Event

Building the next economy met Blockchain en real estate Lelystad Airport, 2 november 2017 Blockchain en real estate Programma Wat is blockchain en waarvoor wordt het gebruikt? BlockchaininRealEstate Blockchain

Building the next economy met Blockchain en real estate Lelystad Airport, 2 november 2017 Blockchain en real estate Programma Wat is blockchain en waarvoor wordt het gebruikt? BlockchaininRealEstate Blockchain

Vertaling Nederlands. Page 1 of 25 INTERNATIONAL STANDARD ON AUDITING 260 COMMUNICATIE MET DE MET GOVERNANCE BELASTE PERSONEN

Engels INTERNATIONAL STANDARD ON AUDITING 260 COMMUNICATION WITH THOSE CHARGED WITH GOVERNANCE (Effective for audits of financial statements for periods beginning on or after December 15, 2009) CONTENTS

Engels INTERNATIONAL STANDARD ON AUDITING 260 COMMUNICATION WITH THOSE CHARGED WITH GOVERNANCE (Effective for audits of financial statements for periods beginning on or after December 15, 2009) CONTENTS

Page 1 of 29. Vertaling NEDERLANDS INTERNATIONAL STANDARD ON AUDITING 210 INTERNATIONAL STANDARD ON AUDITING 210

INTERNATIONAL STANDARD ON AUDITING 210 AGREEING THE TERMS OF AUDIT ENGAGEMENTS (Effective for audits of financial statements for periods beginning on or after December 15, 2009) Introduction Scope of this

INTERNATIONAL STANDARD ON AUDITING 210 AGREEING THE TERMS OF AUDIT ENGAGEMENTS (Effective for audits of financial statements for periods beginning on or after December 15, 2009) Introduction Scope of this

(Big) Data in het sociaal domein

Data in het sociaal domein") (Big) Data in het sociaal domein Congres Sociaal: sturen op gemeentelijke ambities 03-11-2016 Even voorstellen Laudy Konings Lkonings@deloitte.nl 06 1100 3917 Romain Dohmen rdohmen@deloitte.nl 06 2078

(Big) Data in het sociaal domein Congres Sociaal: sturen op gemeentelijke ambities 03-11-2016 Even voorstellen Laudy Konings Lkonings@deloitte.nl 06 1100 3917 Romain Dohmen rdohmen@deloitte.nl 06 2078

4 JULI 2018 Een eerste kennismaking met gemeentefinanciën en verbonden partijen voor raadsleden - vragen

4 JULI 2018 Een eerste kennismaking met gemeentefinanciën en verbonden partijen voor raadsleden - vragen Alkmaar Bergen Castricum Heerhugowaard Heiloo Langedijk Uitgeest Hoe verhoud het EMU saldo zich

4 JULI 2018 Een eerste kennismaking met gemeentefinanciën en verbonden partijen voor raadsleden - vragen Alkmaar Bergen Castricum Heerhugowaard Heiloo Langedijk Uitgeest Hoe verhoud het EMU saldo zich

Our opinion. In our opinion:

Nederlands Let op: dit is een voorbeeldtekst! Engels 00 Voorbeelden oob-controleverklaringen (Controlestandaarden 700-799) 0. Controleverklaringen in overeenstemming met Standaard 702N 0.1.2 Goedkeurende

Nederlands Let op: dit is een voorbeeldtekst! Engels 00 Voorbeelden oob-controleverklaringen (Controlestandaarden 700-799) 0. Controleverklaringen in overeenstemming met Standaard 702N 0.1.2 Goedkeurende

Handleiding Regelgeving Accountancy Engelstalige voorbeeldteksten INHOUD

Handleiding Regelgeving Accountancy Engelstalige voorbeeldteksten INHOUD Deze pdf bevat de volgende Engelstalige voorbeeldrapportages van sectie II, deel 3 HRA: INHOUD 1 0. Controleverklaringen in overeenstemming

Handleiding Regelgeving Accountancy Engelstalige voorbeeldteksten INHOUD Deze pdf bevat de volgende Engelstalige voorbeeldrapportages van sectie II, deel 3 HRA: INHOUD 1 0. Controleverklaringen in overeenstemming

Scope of this ISA 1-3 Reikwijdte van deze ISA 1-3. Effective Date 4 Ingangsdatum 4. Objective 5 Doelstelling 5. Definitions 6-7 Definities 6-7

INTERNATIONAL STANDARD ON AUDITING 800 SPECIAL CONSIDERATIONS AUDITS OF FINANCIAL STATEMENTS PREPARED IN ACCORDANCE WITH SPECIAL PURPOSE FRAMEWORKS (Effective for audits of financial statements for periods

INTERNATIONAL STANDARD ON AUDITING 800 SPECIAL CONSIDERATIONS AUDITS OF FINANCIAL STATEMENTS PREPARED IN ACCORDANCE WITH SPECIAL PURPOSE FRAMEWORKS (Effective for audits of financial statements for periods

Inhoud Deze pdf bevat de volgende Engelstalige voorbeeldrapportages van sectie II, deel 3 HRA:

Handleiding Regelgeving Accountancy Engelstalige voorbeeldteksten Inhoud Deze pdf bevat de volgende Engelstalige voorbeeldrapportages van sectie II, deel 3 HRA: 1.1.1.4: Goedkeurende controleverklaring,

Handleiding Regelgeving Accountancy Engelstalige voorbeeldteksten Inhoud Deze pdf bevat de volgende Engelstalige voorbeeldrapportages van sectie II, deel 3 HRA: 1.1.1.4: Goedkeurende controleverklaring,

2010 Integrated reporting

2010 Integrated reporting Source: Discussion Paper, IIRC, September 2011 1 20/80 2 Source: The International framework, IIRC, December 2013 3 Integrated reporting in eight questions Organizational

2010 Integrated reporting Source: Discussion Paper, IIRC, September 2011 1 20/80 2 Source: The International framework, IIRC, December 2013 3 Integrated reporting in eight questions Organizational

Full disclosure clausule in de overnameovereenkomst. International Law Firm Amsterdam Brussels London Luxembourg New York Rotterdam

Full disclosure clausule in de overnameovereenkomst Wat moet worden begrepen onder full disclosure? - Full disclosure van alle informatie die tussen de verkoper en zijn adviseurs werd overlegd gedurende

Full disclosure clausule in de overnameovereenkomst Wat moet worden begrepen onder full disclosure? - Full disclosure van alle informatie die tussen de verkoper en zijn adviseurs werd overlegd gedurende

Scope of this ISA 1 Reikwijdte van deze ISA 1. Effective Date 2 Ingangsdatum 2. Objectives 3 Doelstellingen 3. Definitions 4 Definities 4

ENGELS INTERNATIONAL STANDARD ON AUDITING 810 ENGAGEMENTS TO REPORT ON SUMMARY FINANCIAL STATEMENTS (Effective for engagements for periods beginning on or after December 15, 2009) Introduction CONTENTS

ENGELS INTERNATIONAL STANDARD ON AUDITING 810 ENGAGEMENTS TO REPORT ON SUMMARY FINANCIAL STATEMENTS (Effective for engagements for periods beginning on or after December 15, 2009) Introduction CONTENTS

Scope of this ISA 1-3 Reikwijdte van deze ISA 1-3. Effective Date 4 Ingangsdatum 4. Objective 5 Doelstelling 5. Definitions 6 Definities 6

INTERNATIONAL STANDARD ON AUDITING 805 SPECIAL CONSIDERATIONS AUDITS OF SINGLE FINANCIAL STATEMENTS AND SPECIFIC ELEMENTS, ACCOUNTS OR ITEMS OF A FINANCIAL STATEMENT Introduction (Effective for audits

INTERNATIONAL STANDARD ON AUDITING 805 SPECIAL CONSIDERATIONS AUDITS OF SINGLE FINANCIAL STATEMENTS AND SPECIFIC ELEMENTS, ACCOUNTS OR ITEMS OF A FINANCIAL STATEMENT Introduction (Effective for audits

Let op: dit is een voorbeeldtekst! 00 Voorbeelden oob-controleverklaringen (Controlestandaarden )

") Nederlands Let op: dit is een voorbeeldtekst! Engels 00 Voorbeelden oob-controleverklaringen (Controlestandaarden 700-799) 0. Controleverklaringen in overeenstemming met Standaard 702N 0.1.3 Goedkeurende

Nederlands Let op: dit is een voorbeeldtekst! Engels 00 Voorbeelden oob-controleverklaringen (Controlestandaarden 700-799) 0. Controleverklaringen in overeenstemming met Standaard 702N 0.1.3 Goedkeurende

Page 1 of 34. Vertaling NEDERLANDS ENGELS

INTERNATIONAL STANDARD ON AUDITING 200 OVERALL OBJECTIVES OF THE INDEPENDENT AUDITOR AND THE CONDUCT OF AN AUDIT IN ACCORDANCE WITH INTERNATIONAL STANDARDS ON AUDITING INTERNATIONAL STANDARD ON AUDITING

INTERNATIONAL STANDARD ON AUDITING 200 OVERALL OBJECTIVES OF THE INDEPENDENT AUDITOR AND THE CONDUCT OF AN AUDIT IN ACCORDANCE WITH INTERNATIONAL STANDARDS ON AUDITING INTERNATIONAL STANDARD ON AUDITING

Lijst met verschillen ISA s versus NV COS 2017

21 april 2017 Status lijst met verschillen Deze publicatie, die tot stand is gekomen onder verantwoordelijkheid van de NBA, geeft de verschillen aan tussen de oorspronkelijke International Standards on

21 april 2017 Status lijst met verschillen Deze publicatie, die tot stand is gekomen onder verantwoordelijkheid van de NBA, geeft de verschillen aan tussen de oorspronkelijke International Standards on

Originally developed by: Translated and re-published by: Royal NBA (The Royal Netherlands Institute of Chartered Accountants)

") Originally developed by: Translated and re-published by: Royal NBA (The Royal Netherlands Institute of Chartered Accountants) ISA 800 (Herzien) Bijzondere overwegingen controles van financiële overzichten

Originally developed by: Translated and re-published by: Royal NBA (The Royal Netherlands Institute of Chartered Accountants) ISA 800 (Herzien) Bijzondere overwegingen controles van financiële overzichten

Luister alsjeblieft naar een opname als je de vragen beantwoordt of speel de stukken zelf!

Martijn Hooning COLLEGE ANALYSE OPDRACHT 1 9 september 2009 Hierbij een paar vragen over twee stukken die we deze week en vorige week hebben besproken: Mondnacht van Schumann, en het eerste deel van het

Martijn Hooning COLLEGE ANALYSE OPDRACHT 1 9 september 2009 Hierbij een paar vragen over twee stukken die we deze week en vorige week hebben besproken: Mondnacht van Schumann, en het eerste deel van het

Value based healthcare door een quality improvement bril

Rotterdam, 7 december 2017 Value based healthcare door een quality improvement bril Ralph So, intensivist en medisch manager Kwaliteit, Veiligheid & Innovatie 16.35-17.00 uur Everybody in healthcare really

Rotterdam, 7 december 2017 Value based healthcare door een quality improvement bril Ralph So, intensivist en medisch manager Kwaliteit, Veiligheid & Innovatie 16.35-17.00 uur Everybody in healthcare really

Revision as the Audit Progresses 12-13 Herziening naarmate de controle vordert 12-13 Documentation 14 Documentatie 14

INTERNATIONAL STANDARD ON AUDITING 320 INTERNATIONAL STANDARD ON AUDITING 320 MATERIALITY IN PLANNING AND PERFORMING AN AUDIT (Effective for audits of financial statements for periods beginning on or after

INTERNATIONAL STANDARD ON AUDITING 320 INTERNATIONAL STANDARD ON AUDITING 320 MATERIALITY IN PLANNING AND PERFORMING AN AUDIT (Effective for audits of financial statements for periods beginning on or after

Page 1 of 19. Vertaling NEDERLANDS INTERNATIONAL STANDARD ON AUDITING 580 INTERNATIONAL STANDARD ON AUDITING 580

CONTENTS Introduction INTERNATIONAL STANDARD ON AUDITING 580 INTERNATIONAL STANDARD ON AUDITING 580 WRITTEN REPRESENTATIONS (Effective for audits of financial statements for periods beginning on or after

CONTENTS Introduction INTERNATIONAL STANDARD ON AUDITING 580 INTERNATIONAL STANDARD ON AUDITING 580 WRITTEN REPRESENTATIONS (Effective for audits of financial statements for periods beginning on or after

INTERNATIONAL STANDARD ON AUDITING 706 INTERNATIONAL STANDARD ON AUDITING 706

INTERNATIONAL STANDARD ON AUDITING 706 INTERNATIONAL STANDARD ON AUDITING 706 EMPHASIS OF MATTER PARAGRAPHS AND OTHER MATTER PARAGRAPHS IN THE INDEPENDENT AUDITOR S REPORT PARAGRAFEN TER BENADRUKKING VAN

INTERNATIONAL STANDARD ON AUDITING 706 INTERNATIONAL STANDARD ON AUDITING 706 EMPHASIS OF MATTER PARAGRAPHS AND OTHER MATTER PARAGRAPHS IN THE INDEPENDENT AUDITOR S REPORT PARAGRAFEN TER BENADRUKKING VAN

Scope of this ISA 1 Toepassingsgebied van deze ISA 1. Effect of Laws and Regulations 2 Invloed van wet- en regelgeving 2

INTERNATIONAL STANDARD ON AUDITING 250 INTERNATIONAL STANDARD ON AUDITING 250 CONSIDERATION OF LAWS AND REGULATIONS IN AN AUDIT OF FINANCIAL STATEMENTS (Effective for audits of financial statements for

INTERNATIONAL STANDARD ON AUDITING 250 INTERNATIONAL STANDARD ON AUDITING 250 CONSIDERATION OF LAWS AND REGULATIONS IN AN AUDIT OF FINANCIAL STATEMENTS (Effective for audits of financial statements for

VOORSTEL TOT STATUTENWIJZIGING UNIQURE NV. Voorgesteld wordt om de artikelen 7.7.1, 8.6.1, en te wijzigen als volgt: Toelichting:

VOORSTEL TOT STATUTENWIJZIGING UNIQURE NV Voorgesteld wordt om de artikelen 7.7.1, 8.6.1, 9.1.2 en 9.1.3 te wijzigen als volgt: Huidige tekst: 7.7.1. Het Bestuur, zomede twee (2) gezamenlijk handelende

VOORSTEL TOT STATUTENWIJZIGING UNIQURE NV Voorgesteld wordt om de artikelen 7.7.1, 8.6.1, 9.1.2 en 9.1.3 te wijzigen als volgt: Huidige tekst: 7.7.1. Het Bestuur, zomede twee (2) gezamenlijk handelende

KPMG PROVADA University 5 juni 2018

IFRS 16 voor de vastgoedsector Ben u er klaar voor? KPMG PROVADA University 5 juni 2018 The concept of IFRS 16 2 IFRS 16 Impact on a lessee s financial statements Balance Sheet IAS 17 (Current Standard)

IFRS 16 voor de vastgoedsector Ben u er klaar voor? KPMG PROVADA University 5 juni 2018 The concept of IFRS 16 2 IFRS 16 Impact on a lessee s financial statements Balance Sheet IAS 17 (Current Standard)

ABLYNX NV. (de Vennootschap of Ablynx )

") ABLYNX NV Naamloze Vennootschap die een openbaar beroep heeft gedaan op het spaarwezen Maatschappelijke zetel: Technologiepark 21, 9052 Zwijnaarde Ondernemingsnummer: 0475.295.446 (RPR Gent) (de Vennootschap

ABLYNX NV Naamloze Vennootschap die een openbaar beroep heeft gedaan op het spaarwezen Maatschappelijke zetel: Technologiepark 21, 9052 Zwijnaarde Ondernemingsnummer: 0475.295.446 (RPR Gent) (de Vennootschap

ISA 260 Communicatie met de met governance belaste personen 7 januari 2016

Originally developed by: Translated and re-published by: Royal NBA (The Royal Netherlands Institute of Chartered Accountants) Dit document maakt gebruik van bladwijzers Translated and re-published by:

Originally developed by: Translated and re-published by: Royal NBA (The Royal Netherlands Institute of Chartered Accountants) Dit document maakt gebruik van bladwijzers Translated and re-published by:

Vertaling NEDERLANDS INTERNATIONAL STANDARD ON AUDITING 560 INTERNATIONAL STANDARD ON AUDITING 560

ENGELS Vertaling NEDERLANDS INTERNATIONAL STANDARD ON AUDITING 560 INTERNATIONAL STANDARD ON AUDITING 560 SUBSEQUENT EVENTS (Effective for audits of financial statements for periods beginning on or after

ENGELS Vertaling NEDERLANDS INTERNATIONAL STANDARD ON AUDITING 560 INTERNATIONAL STANDARD ON AUDITING 560 SUBSEQUENT EVENTS (Effective for audits of financial statements for periods beginning on or after

Vertaling NEDERLANDS INTERNATIONAL STANDARD ON AUDITING 710 INTERNATIONAL STANDARD ON AUDITING 710

ENGELS Vertaling NEDERLANDS INTERNATIONAL STANDARD ON AUDITING 710 INTERNATIONAL STANDARD ON AUDITING 710 COMPARATIVE INFORMATION TER VERGELIJKING OPGENOMEN INFORMATIE CORRESPONDING FIGURES AND COMPARATIVE

ENGELS Vertaling NEDERLANDS INTERNATIONAL STANDARD ON AUDITING 710 INTERNATIONAL STANDARD ON AUDITING 710 COMPARATIVE INFORMATION TER VERGELIJKING OPGENOMEN INFORMATIE CORRESPONDING FIGURES AND COMPARATIVE

Page 1 of 16. Vertaling NEDERLANDS INTERNATIONAL STANDARD ON AUDITING 265 INTERNATIONAL STANDARD ON AUDITING 265

INTERNATIONAL STANDARD ON AUDITING 265 COMMUNICATING DEFICIENCIES IN INTERNAL CONTROL TO THOSE CHARGED WITH GOVERNANCE AND MANAGEMENT (Effective for audits of financial statements for periods beginning

INTERNATIONAL STANDARD ON AUDITING 265 COMMUNICATING DEFICIENCIES IN INTERNAL CONTROL TO THOSE CHARGED WITH GOVERNANCE AND MANAGEMENT (Effective for audits of financial statements for periods beginning

Scope of this ISA 1 Reikwijdte van deze ISA 1. Effect of Laws and Regulations 2 Invloed van wet- en regelgeving 2

INTERNATIONAL STANDARD ON AUDITING 250 CONSIDERATION OF LAWS AND REGULATIONS IN AN AUDIT OF FINANCIAL STATEMENTS (Effective for audits of financial statements for periods beginning on or after December

INTERNATIONAL STANDARD ON AUDITING 250 CONSIDERATION OF LAWS AND REGULATIONS IN AN AUDIT OF FINANCIAL STATEMENTS (Effective for audits of financial statements for periods beginning on or after December

Kennerschap en juridische haken en ogen. Vereniging van Nederlandse Kunsthistorici Amsterdam, 10 juni 2016 R.J.Q. Klomp

Kennerschap en juridische haken en ogen Vereniging van Nederlandse Kunsthistorici Amsterdam, 10 juni 2016 R.J.Q. Klomp De Emmaüsgangers () Lucas 24, 13-35 Juridische haken en ogen Wat te doen als koper

Kennerschap en juridische haken en ogen Vereniging van Nederlandse Kunsthistorici Amsterdam, 10 juni 2016 R.J.Q. Klomp De Emmaüsgangers () Lucas 24, 13-35 Juridische haken en ogen Wat te doen als koper

Scope of this ISA 1 2 Toepassingsgebied van deze ISA 1 2. Effective Date 5 Ingangsdatum 5. Objectives 6 Doelstellingen 6. Definitions 7 Definities 7

INTERNATIONAL STANDARD ON AUDITING 610 INTERNATIONAL STANDARD ON AUDITING 610 USING THE WORK OF INTERNATIONAL AUDITORS GEBRUIKMAKEN VAN DE WERKZAAMHEDEN VAN INTERNE AUDITORS (Effective for audits of financial

INTERNATIONAL STANDARD ON AUDITING 610 INTERNATIONAL STANDARD ON AUDITING 610 USING THE WORK OF INTERNATIONAL AUDITORS GEBRUIKMAKEN VAN DE WERKZAAMHEDEN VAN INTERNE AUDITORS (Effective for audits of financial

General info on using shopping carts with Ingenico epayments

Inhoudsopgave 1. Disclaimer 2. What is a PSPID? 3. What is an API user? How is it different from other users? 4. What is an operation code? And should I choose "Authorisation" or "Sale"? 5. What is an

Inhoudsopgave 1. Disclaimer 2. What is a PSPID? 3. What is an API user? How is it different from other users? 4. What is an operation code? And should I choose "Authorisation" or "Sale"? 5. What is an

Page 1 of 15. Vertaling NEDERLANDS

INTERNATIONAL STANDARD ON AUDITING 450 EVALUATION OF MISSTATEMENTS IDENTIFIED DURING THE AUDIT (Effective for audits of financial statements for periods beginning on or after December 15, 2009) Introduction

INTERNATIONAL STANDARD ON AUDITING 450 EVALUATION OF MISSTATEMENTS IDENTIFIED DURING THE AUDIT (Effective for audits of financial statements for periods beginning on or after December 15, 2009) Introduction

Nieuwe en herziene Standaarden inzake de controleverklaring en wijzigingen in andere Standaarden

Originally developed by: Translated and re-published by: Royal NBA (The Royal Netherlands Institute of Chartered Accountants) Dit document maakt gebruik van bladwijzers Nieuwe en herziene Standaarden inzake

Originally developed by: Translated and re-published by: Royal NBA (The Royal Netherlands Institute of Chartered Accountants) Dit document maakt gebruik van bladwijzers Nieuwe en herziene Standaarden inzake

Originally developed by: Translated and re-published by: Royal NBA (The Royal Netherlands Institute of Chartered Accountants)

") Originally developed by: Translated and re-published by: Royal NBA (The Royal Netherlands Institute of Chartered Accountants) ISA 810 Opdrachten om te rapporteren betreffende samengevatte financiële overzichten

Originally developed by: Translated and re-published by: Royal NBA (The Royal Netherlands Institute of Chartered Accountants) ISA 810 Opdrachten om te rapporteren betreffende samengevatte financiële overzichten

(1) De hoofdfunctie van ons gezelschap is het aanbieden van onderwijs. (2) Ons gezelschap is er om kunsteducatie te verbeteren

De hoofdfunctie van ons gezelschap is het aanbieden van onderwijs. (2) Ons gezelschap is er om kunsteducatie te verbeteren") (1) De hoofdfunctie van ons gezelschap is het aanbieden van onderwijs (2) Ons gezelschap is er om kunsteducatie te verbeteren (3) Ons gezelschap helpt gemeenschappen te vormen en te binden (4) De producties

(1) De hoofdfunctie van ons gezelschap is het aanbieden van onderwijs (2) Ons gezelschap is er om kunsteducatie te verbeteren (3) Ons gezelschap helpt gemeenschappen te vormen en te binden (4) De producties

De impact van automatisering op het Nederlandse onderwijs

De impact van automatisering op het Nederlandse onderwijs Een verkenning op basis van data-analyse Amsterdam, september 2016 Leiden we op tot werkloosheid? De impact van automatisering op het onderwijs

De impact van automatisering op het Nederlandse onderwijs Een verkenning op basis van data-analyse Amsterdam, september 2016 Leiden we op tot werkloosheid? De impact van automatisering op het onderwijs

Bijlage C Onafhankelijkheidsvereisten voor de leden van de raad van commissarissen van Ernst & Young Nederland LLP ( RvC )

") Bijlage C Onafhankelijkheidsvereisten voor de leden van de raad van commissarissen van Ernst & Young Nederland LLP ( RvC ) Uitgangspunten Uitgangspunten bij het borgen van de normen geldend voor de Accountantsorganisatie

Bijlage C Onafhankelijkheidsvereisten voor de leden van de raad van commissarissen van Ernst & Young Nederland LLP ( RvC ) Uitgangspunten Uitgangspunten bij het borgen van de normen geldend voor de Accountantsorganisatie

PRIVACYVERKLARING KLANT- EN LEVERANCIERSADMINISTRATIE

For the privacy statement in English, please scroll down to page 4. PRIVACYVERKLARING KLANT- EN LEVERANCIERSADMINISTRATIE Verzamelen en gebruiken van persoonsgegevens van klanten, leveranciers en andere

For the privacy statement in English, please scroll down to page 4. PRIVACYVERKLARING KLANT- EN LEVERANCIERSADMINISTRATIE Verzamelen en gebruiken van persoonsgegevens van klanten, leveranciers en andere

Originele bron: Handbook of International Standards on Auditing and Quality Control, 2015 Edition - ISBN number:

INTERNATIONAL STANDARD ON AUDITING (ISA) ISA 720 (Herzien), De verantwoordelijkheden van de auditor met betrekking tot andere informatie Copyright IFAC Deze Internationale controlestandaard (ISA) werd

INTERNATIONAL STANDARD ON AUDITING (ISA) ISA 720 (Herzien), De verantwoordelijkheden van de auditor met betrekking tot andere informatie Copyright IFAC Deze Internationale controlestandaard (ISA) werd

Quality of life in persons with profound intellectual and multiple disabilities. Marga Nieuwenhuijse maart 2016

Quality of life in persons with profound intellectual and multiple disabilities Marga Nieuwenhuijse maart 2016 Beoogde resultaten Literatuuronderzoek naar de bestaande concepten van kwaliteit van leven

Quality of life in persons with profound intellectual and multiple disabilities Marga Nieuwenhuijse maart 2016 Beoogde resultaten Literatuuronderzoek naar de bestaande concepten van kwaliteit van leven

De beleidsrobot. Realiteit of illusie?

De beleidsrobot Realiteit of illusie? In een minuut.. 2017 Deloitte The Netherlands Insert your footer here De mogelijkheden van analytics nemen snel toe.. Data Informatie Inzicht Beschrijvend Wat is er

De beleidsrobot Realiteit of illusie? In een minuut.. 2017 Deloitte The Netherlands Insert your footer here De mogelijkheden van analytics nemen snel toe.. Data Informatie Inzicht Beschrijvend Wat is er

Disclosure belangen spreker

Disclosure belangen spreker (potentiële) belangenverstrengeling Voor bijeenkomst mogelijk relevante relaties met bedrijven Sponsoring of onderzoeksgeld Honorarium of andere (financiële) vergoeding Aandeelhouder

Disclosure belangen spreker (potentiële) belangenverstrengeling Voor bijeenkomst mogelijk relevante relaties met bedrijven Sponsoring of onderzoeksgeld Honorarium of andere (financiële) vergoeding Aandeelhouder

Page 1 of 18. Vertaling NEDERLANDS. (Effective for audits of financial statements for periods beginning on or after December 15, 2009)

") ENGELS INTERNATIONAL STANDARD ON AUDITING 570 GOING CONCERN (Effective for audits of financial statements for periods beginning on or after December 15, 2009) Introduction Scope of this ISA 1 Going Concern

ENGELS INTERNATIONAL STANDARD ON AUDITING 570 GOING CONCERN (Effective for audits of financial statements for periods beginning on or after December 15, 2009) Introduction Scope of this ISA 1 Going Concern

Inhoud Deze PDF bevat de drukproef van de volgende Engelstalige voorbeeldrapportages uit HRA dele 3:

Handleiding Regelgeving Accountancy Engelstalige voorbeeldteksten Inhoud Deze PDF bevat de drukproef van de volgende Engelstalige voorbeeldrapportages uit HRA dele 3: 2-serie: Various review reports 3-serie:

Handleiding Regelgeving Accountancy Engelstalige voorbeeldteksten Inhoud Deze PDF bevat de drukproef van de volgende Engelstalige voorbeeldrapportages uit HRA dele 3: 2-serie: Various review reports 3-serie:

Chapter 4 Understanding Families. In this chapter, you will learn

Chapter 4 Understanding Families In this chapter, you will learn Topic 4-1 What Is a Family? In this topic, you will learn about the factors that make the family such an important unit, as well as Roles

Chapter 4 Understanding Families In this chapter, you will learn Topic 4-1 What Is a Family? In this topic, you will learn about the factors that make the family such an important unit, as well as Roles

Dit document maakt gebruik van bladwijzers.

Originally developed by: Translated and re-published by: Royal NBA (The Royal Netherlands Institute of Chartered Accountants) Dit document maakt gebruik van bladwijzers. ISA 720 De verantwoordelijkheden

Originally developed by: Translated and re-published by: Royal NBA (The Royal Netherlands Institute of Chartered Accountants) Dit document maakt gebruik van bladwijzers. ISA 720 De verantwoordelijkheden

Our disclaimer of opinion

Nederlands Let op: dit is een voorbeeldtekst! Engels 00 Voorbeelden oob-controleverklaringen (Controlestandaarden 700-799) 0. Controleverklaringen in overeenstemming met Standaard 702N 0.1.13 Controleverklaring

Nederlands Let op: dit is een voorbeeldtekst! Engels 00 Voorbeelden oob-controleverklaringen (Controlestandaarden 700-799) 0. Controleverklaringen in overeenstemming met Standaard 702N 0.1.13 Controleverklaring

Optional client logo (Smaller than Deloitte logo) State of the State

State of the State") Optional client logo (Smaller than Deloitte logo) State of the State Den Haag 28 maart 2017 State of the State - Presentatie Taxlab 1 plancapaciteit hebben dan de veronderstelde huishoudensgroei. State

Optional client logo (Smaller than Deloitte logo) State of the State Den Haag 28 maart 2017 State of the State - Presentatie Taxlab 1 plancapaciteit hebben dan de veronderstelde huishoudensgroei. State

My Benefits My Choice applicatie. Registratie & inlogprocedure

My Benefits My Choice applicatie Registratie & inlogprocedure Welkom bij de My Benefits My Choice applicatie Gezien de applicatie gebruik maakt van uw persoonlijke gegevens en salarisinformatie wordt de

My Benefits My Choice applicatie Registratie & inlogprocedure Welkom bij de My Benefits My Choice applicatie Gezien de applicatie gebruik maakt van uw persoonlijke gegevens en salarisinformatie wordt de

Inhoud Deze pdf bevat de volgende Engelstalige voorbeeldrapportages van sectie II, deel 3 HRA:

Handleiding Regelgeving Accountancy Engelstalige voorbeeldteksten Inhoud Deze pdf bevat de volgende Engelstalige voorbeeldrapportages van sectie II, deel 3 HRA: 2-serie: 3-serie: 4-serie: 5-serie: 7-serie:

Handleiding Regelgeving Accountancy Engelstalige voorbeeldteksten Inhoud Deze pdf bevat de volgende Engelstalige voorbeeldrapportages van sectie II, deel 3 HRA: 2-serie: 3-serie: 4-serie: 5-serie: 7-serie:

Consultatiedocument: Vertaling herziene Standaard 720 Respondent: Dhr. G. Wolswijk Datum inzending: 27 januari 2016

Consultatiedocument: Vertaling herziene Standaard 720 Respondent: Dhr. G. Wolswijk Datum inzending: 27 januari 2016 LS, Op persoonlijke titel reageer ik hierbij op de consultatie rond de herziene standaard

Consultatiedocument: Vertaling herziene Standaard 720 Respondent: Dhr. G. Wolswijk Datum inzending: 27 januari 2016 LS, Op persoonlijke titel reageer ik hierbij op de consultatie rond de herziene standaard

Gezien de commentaren ontvangen op deze openbare raadpleging;

Ontwerp van norm inzake de toepassing van de nieuwe en herziene Internationale controlestandaarden (ISA s) in België en tot vervanging van de norm van 10 november 2009 inzake de toepassing van de ISA s

Ontwerp van norm inzake de toepassing van de nieuwe en herziene Internationale controlestandaarden (ISA s) in België en tot vervanging van de norm van 10 november 2009 inzake de toepassing van de ISA s

RECEPTEERKUNDE: PRODUCTZORG EN BEREIDING VAN GENEESMIDDELEN (DUTCH EDITION) FROM BOHN STAFLEU VAN LOGHUM

FROM BOHN STAFLEU VAN LOGHUM") Read Online and Download Ebook RECEPTEERKUNDE: PRODUCTZORG EN BEREIDING VAN GENEESMIDDELEN (DUTCH EDITION) FROM BOHN STAFLEU VAN LOGHUM DOWNLOAD EBOOK : RECEPTEERKUNDE: PRODUCTZORG EN BEREIDING VAN STAFLEU

Read Online and Download Ebook RECEPTEERKUNDE: PRODUCTZORG EN BEREIDING VAN GENEESMIDDELEN (DUTCH EDITION) FROM BOHN STAFLEU VAN LOGHUM DOWNLOAD EBOOK : RECEPTEERKUNDE: PRODUCTZORG EN BEREIDING VAN STAFLEU

COMMISSIE VOOR BOEKHOUDKUNDIGE NORMEN

COMMISSIE VOOR BOEKHOUDKUNDIGE NORMEN DE INTERPRETATIE VAN DE OPENBAARMAKINGSVERPLICHTING VAN TRANSACTIES VAN ENIGE BETEKENIS MET VERBONDEN PARTIJEN BUITEN NORMALE MARKTVOORWAARDEN, ZOALS BEPAALD IN HET

COMMISSIE VOOR BOEKHOUDKUNDIGE NORMEN DE INTERPRETATIE VAN DE OPENBAARMAKINGSVERPLICHTING VAN TRANSACTIES VAN ENIGE BETEKENIS MET VERBONDEN PARTIJEN BUITEN NORMALE MARKTVOORWAARDEN, ZOALS BEPAALD IN HET

Elektronisch handtekenen in een handomdraai! Het proces in enkele stappen 2017, Deloitte Accountancy

Elektronisch handtekenen in een handomdraai! Het proces in enkele stappen 2017, Deloitte Accountancy Onderteken op elk moment! Waarom elektronisch ondertekenen zo gemakkelijk is Zoals u weet gaat het ondertekenen

Elektronisch handtekenen in een handomdraai! Het proces in enkele stappen 2017, Deloitte Accountancy Onderteken op elk moment! Waarom elektronisch ondertekenen zo gemakkelijk is Zoals u weet gaat het ondertekenen

INTERNATIONAL STANDARD ON AUDITING (ISA)

") INTERNATIONAL STANDARD ON AUDITING (ISA) ISA 5 7 0 (Herzien), Continuïteit Copyright IFAC Deze Internationale controlestandaard (ISA) werd in 2015 in de Engelse taal gepubliceerd door de International

INTERNATIONAL STANDARD ON AUDITING (ISA) ISA 5 7 0 (Herzien), Continuïteit Copyright IFAC Deze Internationale controlestandaard (ISA) werd in 2015 in de Engelse taal gepubliceerd door de International

Cambridge Assessment International Education Cambridge International General Certificate of Secondary Education. Published

Cambridge Assessment International Education Cambridge International General Certificate of Secondary Education DUTCH 055/02 Paper 2 Reading MARK SCHEME Maximum Mark: 45 Published This mark scheme is published

Cambridge Assessment International Education Cambridge International General Certificate of Secondary Education DUTCH 055/02 Paper 2 Reading MARK SCHEME Maximum Mark: 45 Published This mark scheme is published

Bouwen aan vertrouwen: perspectief van de industrie

Symposium ter gelegenheid afscheid Ad van Dooren Zelfredzaamheid van patiënten bij gebruik van veilige medicatie. Bouwen aan vertrouwen: perspectief van de industrie Rudolf van Olden, arts Medisch Directeur

Symposium ter gelegenheid afscheid Ad van Dooren Zelfredzaamheid van patiënten bij gebruik van veilige medicatie. Bouwen aan vertrouwen: perspectief van de industrie Rudolf van Olden, arts Medisch Directeur

Business Opening. Very formal, recipient has a special title that must be used in place of their name

- Opening Geachte heer President Geachte heer President Very formal, recipient has a special title that must be used in place of their name Geachte heer Formal, male recipient, name unknown Geachte mevrouw

- Opening Geachte heer President Geachte heer President Very formal, recipient has a special title that must be used in place of their name Geachte heer Formal, male recipient, name unknown Geachte mevrouw

Topic 10-5 Meeting Children s Intellectual Needs

Topic 10-5 Meeting Children s Intellectual Needs In this topic, you will learn how to help children develop the ability to reason and use complex thought, as well as The role of play in intellectual development

Topic 10-5 Meeting Children s Intellectual Needs In this topic, you will learn how to help children develop the ability to reason and use complex thought, as well as The role of play in intellectual development

Netherlands Ministry of Spatial Planning, Housing and the Environment. Internet practices

Netherlands Ministry of Spatial Planning, Housing and the Environment Internet practices What have we learned so far? A short history Aims and uses of our site: www.vrom.nl Our international internet communications

Netherlands Ministry of Spatial Planning, Housing and the Environment Internet practices What have we learned so far? A short history Aims and uses of our site: www.vrom.nl Our international internet communications

EU Data Protection Wetgeving

Fundamentals of data protection EU Data Protection Wetgeving Prof. Paul de Hert Vrije Universiteit Brussel (LSTS) 1 Outline -overzicht -drie fundamenten -recente uitspraak Hof van Justitie Recht op data

Fundamentals of data protection EU Data Protection Wetgeving Prof. Paul de Hert Vrije Universiteit Brussel (LSTS) 1 Outline -overzicht -drie fundamenten -recente uitspraak Hof van Justitie Recht op data

COMMISSIE VAN DE EUROPESE GEMEENSCHAPPEN. Voorstel voor een VERORDENING VAN DE RAAD

COMMISSIE VAN DE EUROPESE GEMEENSCHAPPEN w w Brussel, 22.12.2004 COM(2004) 822 definitief 2004/0282 (ACC) Voorstel voor een VERORDENING VAN DE RAAD tot wijziging en tot opschorting van de toepassing van

COMMISSIE VAN DE EUROPESE GEMEENSCHAPPEN w w Brussel, 22.12.2004 COM(2004) 822 definitief 2004/0282 (ACC) Voorstel voor een VERORDENING VAN DE RAAD tot wijziging en tot opschorting van de toepassing van

Paragraph. Effective Date 5 Ingangsdatum 5. Objectives 6 Doelstellingen 6. Definitions 7 Definities 7

ISA 610 v0.1 INTERNATIONAL STANDARD ON AUDITING 610 USING THE WORK OF INTERNAL AUDITORS (Effective for audits of financial statements for periods beginning on or after December 15, 2009) CONTENTS Paragraph

ISA 610 v0.1 INTERNATIONAL STANDARD ON AUDITING 610 USING THE WORK OF INTERNAL AUDITORS (Effective for audits of financial statements for periods beginning on or after December 15, 2009) CONTENTS Paragraph

DEPARTMENT OF ENVIRONMENTAL AFFAIRS NOTICE 245 OF 2017

Environmental Affairs, Department of/ Omgewingsake, Departement van 245 National Environmental Management Laws Amendment Bill, 2017: Explanatory summary of the Act 40733 STAATSKOERANT, 31 MAART 2017 No.

Environmental Affairs, Department of/ Omgewingsake, Departement van 245 National Environmental Management Laws Amendment Bill, 2017: Explanatory summary of the Act 40733 STAATSKOERANT, 31 MAART 2017 No.

Besluitenlijst CCvD HACCP/ List of decisions National Board of Experts HACCP

Besluitenlijst CCvD HACCP/ List of decisions National Board of Experts HACCP Dit is de actuele besluitenlijst van het CCvD HACCP. Op deze besluitenlijst staan alle relevante besluiten van het CCvD HACCP

Besluitenlijst CCvD HACCP/ List of decisions National Board of Experts HACCP Dit is de actuele besluitenlijst van het CCvD HACCP. Op deze besluitenlijst staan alle relevante besluiten van het CCvD HACCP

ROULATIE VAN AUDITKANTOREN: Nederlands wetsontwerp en toelichting daarop strijdig met Europese wetgeving

ADVOCATEN NOTARISSEN BELASTINGADVISEURS Amsterdam, 17 september 2015 Memorandum ROULATIE VAN AUDITKANTOREN: Nederlands wetsontwerp en toelichting daarop strijdig met Europese wetgeving Conclusie Om redenen

ADVOCATEN NOTARISSEN BELASTINGADVISEURS Amsterdam, 17 september 2015 Memorandum ROULATIE VAN AUDITKANTOREN: Nederlands wetsontwerp en toelichting daarop strijdig met Europese wetgeving Conclusie Om redenen

Het betreft hier aanpassingen aan Standaard 315 i.v.m. het herzien van Standaard 610. Consultatieperiode loopt tot 11 november 2013, 14.

Originally developed by: Translated and re-published by: NBA (The Netherlands Institute of Chartered Accountants) Concept Standaard 315 Risico s op een afwijking van materieel belang identificeren en inschatten

Originally developed by: Translated and re-published by: NBA (The Netherlands Institute of Chartered Accountants) Concept Standaard 315 Risico s op een afwijking van materieel belang identificeren en inschatten

ANGSTSTOORNISSEN EN HYPOCHONDRIE: DIAGNOSTIEK EN BEHANDELING (DUTCH EDITION) FROM BOHN STAFLEU VAN LOGHUM

FROM BOHN STAFLEU VAN LOGHUM") Read Online and Download Ebook ANGSTSTOORNISSEN EN HYPOCHONDRIE: DIAGNOSTIEK EN BEHANDELING (DUTCH EDITION) FROM BOHN STAFLEU VAN LOGHUM DOWNLOAD EBOOK : ANGSTSTOORNISSEN EN HYPOCHONDRIE: DIAGNOSTIEK STAFLEU

Read Online and Download Ebook ANGSTSTOORNISSEN EN HYPOCHONDRIE: DIAGNOSTIEK EN BEHANDELING (DUTCH EDITION) FROM BOHN STAFLEU VAN LOGHUM DOWNLOAD EBOOK : ANGSTSTOORNISSEN EN HYPOCHONDRIE: DIAGNOSTIEK STAFLEU

Ctrl Ketenoptimalisatie Slimme automatisering en kostenreductie

Ctrl Ketenoptimalisatie Slimme automatisering en kostenreductie 1 Ctrl - Ketenoptimalisatie Technische hype cycles 2 Ctrl - Ketenoptimalisatie Technologische trends en veranderingen Big data & internet

Ctrl Ketenoptimalisatie Slimme automatisering en kostenreductie 1 Ctrl - Ketenoptimalisatie Technische hype cycles 2 Ctrl - Ketenoptimalisatie Technologische trends en veranderingen Big data & internet

Vertaling NEDERLANDS INTERNATIONAL STANDARD ON AUDITING 402. Paragraph. Inleiding

INTERNATIONAL STANDARD ON AUDITING 402 AUDIT CONSIDERATIONS RELATING TO AN ENTITY USING A SERVICE ORGANIZATION (Effective for audits of financial statements for periods beginning on or after December 15,

INTERNATIONAL STANDARD ON AUDITING 402 AUDIT CONSIDERATIONS RELATING TO AN ENTITY USING A SERVICE ORGANIZATION (Effective for audits of financial statements for periods beginning on or after December 15,

DECLARATION FOR GAD approval

Version 1.2 DECLARATION FOR GAD approval Declare that for the following central heating boilers Intergas Calderas de Calefacción S. L. Kombi Kompakt R 24, 28/24, 36/30 and Prestige The installation and

Version 1.2 DECLARATION FOR GAD approval Declare that for the following central heating boilers Intergas Calderas de Calefacción S. L. Kombi Kompakt R 24, 28/24, 36/30 and Prestige The installation and

Buy Me FILE 5 BUY ME BK 2

Buy Me FILE BUY ME BK Can you resist all those incredible products that all seem to be screaming: Buy Me! Every day we see them on TV during the commercial break: the best products in the world. How would

Buy Me FILE BUY ME BK Can you resist all those incredible products that all seem to be screaming: Buy Me! Every day we see them on TV during the commercial break: the best products in the world. How would

WEGWIJZER VOOR METHODEN BIJ PROJECTMANAGEMENT (PROJECT MANAGEMENT) (DUTCH EDITION) BY EDWIN BAARDMAN, GERARD BAKKER, JAN VAN BEIJNHEM, FR

(DUTCH EDITION) BY EDWIN BAARDMAN, GERARD BAKKER, JAN VAN BEIJNHEM, FR") Read Online and Download Ebook WEGWIJZER VOOR METHODEN BIJ PROJECTMANAGEMENT (PROJECT MANAGEMENT) (DUTCH EDITION) BY EDWIN BAARDMAN, GERARD BAKKER, JAN VAN BEIJNHEM, FR DOWNLOAD EBOOK : WEGWIJZER VOOR

Read Online and Download Ebook WEGWIJZER VOOR METHODEN BIJ PROJECTMANAGEMENT (PROJECT MANAGEMENT) (DUTCH EDITION) BY EDWIN BAARDMAN, GERARD BAKKER, JAN VAN BEIJNHEM, FR DOWNLOAD EBOOK : WEGWIJZER VOOR

SAMPLE 11 = + 11 = + + Exploring Combinations of Ten + + = = + + = + = = + = = 11. Step Up. Step Ahead

7.1 Exploring Combinations of Ten Look at these cubes. 2. Color some of the cubes to make three parts. Then write a matching sentence. 10 What addition sentence matches the picture? How else could you

7.1 Exploring Combinations of Ten Look at these cubes. 2. Color some of the cubes to make three parts. Then write a matching sentence. 10 What addition sentence matches the picture? How else could you

0515 DUTCH (FOREIGN LANGUAGE)

") UNIVERSITY OF CAMBRIDGE INTERNATIONAL EXAMINATIONS International General Certificate of Secondary Education MARK SCHEME for the May/June 2011 question paper for the guidance of teachers 0515 DUTCH (FOREIGN

UNIVERSITY OF CAMBRIDGE INTERNATIONAL EXAMINATIONS International General Certificate of Secondary Education MARK SCHEME for the May/June 2011 question paper for the guidance of teachers 0515 DUTCH (FOREIGN

Verantwoording en controle in het Sociaal Domein. Drs. A.B. (Toby) Bergshoeff RA 17 november 2016

Bergshoeff RA 17 november 2016") Verantwoording en controle in het Sociaal Domein Drs. A.B. (Toby) Bergshoeff RA 17 november 2016 Agenda Verantwoording en controle in het Sociaal Domein 1. Terugblik 2015 Ruim 50% van de gemeenten geen

Verantwoording en controle in het Sociaal Domein Drs. A.B. (Toby) Bergshoeff RA 17 november 2016 Agenda Verantwoording en controle in het Sociaal Domein 1. Terugblik 2015 Ruim 50% van de gemeenten geen

Understanding and being understood begins with speaking Dutch

Understanding and being understood begins with speaking Dutch Begrijpen en begrepen worden begint met het spreken van de Nederlandse taal The Dutch language links us all Wat leest u in deze folder? 1.

Understanding and being understood begins with speaking Dutch Begrijpen en begrepen worden begint met het spreken van de Nederlandse taal The Dutch language links us all Wat leest u in deze folder? 1.

Extreem veilig Het product Our product Voordeel Advantage Bajolock Bajolock Bajolock Bajolock Bajolock Bajolock Bajolock

Extreem veilig Het product Alle koppeling zijn speciaal ontworpen en vervaardigd uit hoogwaardig RVS 316L en uitgevoerd met hoogwaardige pakkingen. Op alle koppelingen zorgt het gepatenteerde veiligheid

Extreem veilig Het product Alle koppeling zijn speciaal ontworpen en vervaardigd uit hoogwaardig RVS 316L en uitgevoerd met hoogwaardige pakkingen. Op alle koppelingen zorgt het gepatenteerde veiligheid

Nieuwe en herziene Standaarden inzake de controleverklaring en wijzigingen in andere Standaarden

Originally developed by: Translated and re-published by: Royal NBA (The Royal Netherlands Institute of Chartered Accountants) Dit document maakt gebruik van bladwijzers Nieuwe en herziene Standaarden inzake

Originally developed by: Translated and re-published by: Royal NBA (The Royal Netherlands Institute of Chartered Accountants) Dit document maakt gebruik van bladwijzers Nieuwe en herziene Standaarden inzake

Over cloud-computing en Europese privacywetgeving: nu en straks

SURFNET SEMINAR PRIVACY & DE CLOUD: DE STAND VAN ZAKEN Over cloud-computing en Europese privacywetgeving: nu en straks Gerrit-Jan Zwenne Utrecht 26 juni 2012 roadmap privacyrichtlijn 95/46/EG - verantwoordelijke

SURFNET SEMINAR PRIVACY & DE CLOUD: DE STAND VAN ZAKEN Over cloud-computing en Europese privacywetgeving: nu en straks Gerrit-Jan Zwenne Utrecht 26 juni 2012 roadmap privacyrichtlijn 95/46/EG - verantwoordelijke

Global TV Canada s Pulse 2011

Global TV Canada s Pulse 2011 Winnipeg Nobody s Unpredictable Methodology These are the findings of an Ipsos Reid poll conducted between August 26 to September 1, 2011 on behalf of Global Television. For

Global TV Canada s Pulse 2011 Winnipeg Nobody s Unpredictable Methodology These are the findings of an Ipsos Reid poll conducted between August 26 to September 1, 2011 on behalf of Global Television. For

DE ALGEMENE VERORDENING GEGEVENSBESCHERMING

ELAW BASISCURSUS WBP EN ANDERE PRIVACYWETGEVING DE ALGEMENE VERORDENING GEGEVENSBESCHERMING Gerrit-Jan Zwenne 28 november 2013 general data protection regulation een snelle vergelijking DP Directive 95/46/EC

ELAW BASISCURSUS WBP EN ANDERE PRIVACYWETGEVING DE ALGEMENE VERORDENING GEGEVENSBESCHERMING Gerrit-Jan Zwenne 28 november 2013 general data protection regulation een snelle vergelijking DP Directive 95/46/EC

IFRS 15 Disaggregatie van opbrengsten

IFRS 15 Disaggregatie van opbrengsten Ralph ter Hoeven Partner Professional Practice Department +31 (0) 8 8288 1080 +31 (0) 6 2127 2327 rterhoeven@deloitte.nl Dingeman Manschot Director Professional Practice

IFRS 15 Disaggregatie van opbrengsten Ralph ter Hoeven Partner Professional Practice Department +31 (0) 8 8288 1080 +31 (0) 6 2127 2327 rterhoeven@deloitte.nl Dingeman Manschot Director Professional Practice

04/11/2013. Sluitersnelheid: 1/50 sec = 0.02 sec. Frameduur= 2 x sluitersnelheid= 2/50 = 1/25 = 0.04 sec. Framerate= 1/0.

Onderwerpen: Scherpstelling - Focusering Sluitersnelheid en framerate Sluitersnelheid en belichting Driedimensionale Arthrokinematische Mobilisatie Cursus Klinische Video/Foto-Analyse Avond 3: Scherpte

Onderwerpen: Scherpstelling - Focusering Sluitersnelheid en framerate Sluitersnelheid en belichting Driedimensionale Arthrokinematische Mobilisatie Cursus Klinische Video/Foto-Analyse Avond 3: Scherpte

CONTENTS INHOUDSOPGAVE

INTERNATIONAL STANDARD ON AUDITING 240 THE AUDITOR S RESPONSIBILITIES RELATING TO FRAUD IN AN AUDIT OF FINANCIAL STATEMENTS (Effective for audits of financial statements for periods beginning on or after

INTERNATIONAL STANDARD ON AUDITING 240 THE AUDITOR S RESPONSIBILITIES RELATING TO FRAUD IN AN AUDIT OF FINANCIAL STATEMENTS (Effective for audits of financial statements for periods beginning on or after

De voorzitter van de Tweede Kamer der Staten-Generaal Postbus 20018 2500 EA DEN HAAG. Datum 21 januari 2014 Betreft Kamervragen. Geachte voorzitter,

> Retouradres Postbus 20350 2500 EJ Den Haag De voorzitter van de Tweede Kamer der Staten-Generaal Postbus 2008 2500 EA DEN HAAG Bezoekadres: Rijnstraat 50 255 XP DEN HAAG T 070 340 79 F 070 340 78 34

> Retouradres Postbus 20350 2500 EJ Den Haag De voorzitter van de Tweede Kamer der Staten-Generaal Postbus 2008 2500 EA DEN HAAG Bezoekadres: Rijnstraat 50 255 XP DEN HAAG T 070 340 79 F 070 340 78 34

Raadsman bij het politieverhoor

De Nederlandse situatie J. Boksem Leuven, 23 april 2009 Lange voorgeschiedenis o.a: C. Fijnaut EHRM Schiedammer Parkmoord Verbeterprogramma Motie Dittrich: overwegende dat de kwaliteit van het politieverhoor

De Nederlandse situatie J. Boksem Leuven, 23 april 2009 Lange voorgeschiedenis o.a: C. Fijnaut EHRM Schiedammer Parkmoord Verbeterprogramma Motie Dittrich: overwegende dat de kwaliteit van het politieverhoor