Master Thesis: Revenue Model Innovation for (Dutch) Strategic Consultants in an International Environment.

|

|

|

- Franciscus Veenstra

- 8 jaren geleden

- Aantal bezoeken:

Transcriptie

1 Zwolle, May 2013 Master Thesis: Revenue Model Innovation for (Dutch) Strategic Consultants in an International Environment. by Ernst Vossers B.Eng Automotive Engineering Student identity number in partial fulfillment of the requirements for the degree of Master of Science in Innovation Management Supervisors: dr. U. Konus, TU/e, ITEM dr. J.J.L. Schepers TU/e, ITEM 1

2 TUE. School of Industrial Engineering. Series Master Theses Innovation Management Subject headings: Business Model Innovation, Revenue Model Innovation, Internationalization, Barriers for Internationalization, Strategic consultancy, Professional Service Firms. 2

3 Table of Contents Table of Figures... 5 Table of Tables... 5 List of Abbreviations... 6 Management Summary... 7 Preface / Acknowledgements Introduction Inducement for the research Personal Inducement for the research Definitions Problem definition Research objective Main research question Research questions Relevance Report Outline Research Methodology Research classification Research strategy Unit of analysis Part 1 Literature review Part 2, Case study Selection of the cases Data collection Interviews Data analysis Research quality Part 1 Literature Review Theoretical background Strategic Consultancy Business Models Business Model Framework Business Model Development Business (Revenue) Models of Consultants Business (Revenue) Model Innovation Barriers for Business and Revenue Model Innovation Discussion and conclusion of the literature review

4 Part 2 Field Research Results and Analysis Introduction Case Descriptions Presentation of results Results Revenue Model Innovation (International) Barriers for revenue model Innovation (Q2) (International) Revenue model innovation risks (Q3) Revenue Model Innovation Opportunities (Q1) Costs (Q1A) Revenue stream (Q1B) Analysis Revenue Model Innovation Framework Conclusion Discussion Managerial Implications Limitations Bibliography Appendix I Appendix II Appendix III Appendix IV Appendix V Appendix VI Appendix VII Appendix IIX Appendix IX Appendix X Appendix XI Appendix XII Appendix XIIV Appendix XIV Appendix XV Appendix XVI Appendix XVII

5 Table of Figures Figure 1 Research objective Figure 2 Reflective cycle Figure 3 Policy Cycle Figure 4 Business Triangle, (Osterwalder et al., 2005) Figure 5 Business model blocks linkage Figure 6 Pricing factors, (Owusu-Manu et al., 2012) Figure 7 Revenue model innovation appropriate? Figure 8 Revenue model innovation framework Figure 9 Offices ARCADIS Figure 10 Top 10 design firms Figure 11 Osterwalder and Pigneur s BMC Figure 12 Patrick Stähler, Revised BMC Figure 13 Value Proposition Canvas and Business model Canvas Figure 14 Business model innovation epicenters Figure 15 Six dimensional model of service innovation and the dynamic capabilities for realizing new service experiences and solutions Figure 16 Business Model Innovation according to IBM Figure 17 Successful business model innovation results Figure 18 Fee range according to project complexity, APPEGA Figure 19 The value of new revenue models in public firms Figure 20 Barriers for internationalization Figure 21 Revenue model innovation Figure 22 Earnings Model Game Table of Tables Table 1 Function overview of interviewees Table 2 Factor identification Table 3 Barriers identified Table 4 Risks for revenue model innovation Table 5 Revenue model innovation opportunities Table 6 Explanation of the factors of the general model Table 7 Types of consulting services Table 8 Change opportunities costs Table 9 Clients of consultancy firms

6 List of Abbreviations PSF BMC CEO SCA CA S&B D&R R&D CSR OPCO SME MNE MNC EU GDP B2B B2C EPC D&C DBFM(O) PPS T&G NS VRM DTG TUe ZZP OLI FDI VPC BMF Professional Service Firm Business Model Canvas Chief Executive Officer Sustainable Competitive Advantage Competitive Advantage Department of ARCADIS: Strategy and Policy making Department of ARCADIS: Delta s and Rivers Research and Development Case Study Research Operating Company Small and Medium Enterprise Multi National Enterprise Multi National Client European Union Gross Domestic Product Business to Business Business to Consumer Engineering-Procurement-Construction Design & Construct Design, Build, Finance, Maintain, (Operate) Public Private Collaboration (publiek private samenwerking) Twynstra & Gudde Dutch Railroads: Nederlandse Spoorwegen Value Reference Model Deutsche Treuhand-Gesellschaft Technical University Eindhoven Dutch: Zelstandige Zonder Personeel Ownership Location Internalization Foreign Direct Inverstment Value Proposition Canvas Business Model Framework 6

Public Private Collaboration (publiek private samenwerking) Twynstra & Gudde Dutch Railroads:")

7 Management Summary In current competitive environment firms need to be able to adapt their-self s successfully in a short period of time. Moore (2008) states that innovation and continual adaptation is essential for the survival of organizations. This adaptation can often be found in business and revenue models. Wirtz et al., (2010) support this with their finding that firms have to innovate their business models constantly if they want to match the needs of the market, be unique and optimize the value delivered. Further there is relatively little known about how firms (and thus managers) can go about achieving this transformation, and how, and to what extent, different types of business models should be adapted. Developing and adapting their firm s business model has become a major task for many executives in their efforts to cope successfully with technological progress, competitive changes, or governmental and regulatory alterations (Wirtz et al., (2010), pg 2). According to Teece (2009) a business model demonstrates how a business creates and delivers value to customers. This value delivered is outlined by elaborating the revenues, costs, and profits associated with the business enterprise delivering that value. The cost, revenue streams and profits are representing the revenue model. This research is aiming to provide insights how revenue model innovation successfully can be used by strategic consultants in their international environment. The main research question is therefore: What changes in the revenue model need to be made in order to be successful as strategic consultant in an international environment? This topic is currently under researched and thus the amount of quantitative data is limited. Therefore this qualitative and explorative research serves as a starting point for further quantitative research. In order to do so, a general framework (Figure 8) is developed that can be further tested by other researchers. To provide meaningful insights and to ensure relevance, ARCADIS (a major player on environmental consultancy and engineering) offered the opportunity to conduct the research at their advisory Strategy and Decision making. The research question was addressed by means of case study research and therefore 8 distinctive cases are developed by interviewing several experts (consultants). In order to ensure the academic quality of the research, the reflective cycle of Van Aken et al., (2007), as shown in Figure 2, is used. Trends and developments are identified with use of the findings of the literature review and the findings from the interviews. It needs to be remarked that the answer on this question goes further than just a few things that need to be changed in the revenue model itself. This answer would be relative straightforward, namely the cost or the revenues need to be changed. This implies minimizing cost and maximizing revenues with use of several interventions in the current business process of strategic consultants. For both, this is not possible without developing a good offer (value proposition). Moreover this value proposition or offer is 7

can go about achieving this transformation, and how, and to what extent, different types of business models should be")

8 regarded as the heart of the business model, and therefore it influences the revenue model (Osterwalder and Pigneur 2010). The direct and indirect costs of revenue models can be innovated. The pricing model, the pricing methodology, the payment structure, pricing strategy and payment timing are opportunities to innovate the revenue streams on. The revenue streams offer more opportunities for these firms to innovate on then the costs offer. The direct costs of consultants are rather stable in their home environment, thus only by leveraging these additional revenues can be gathered. In contrast to the direct costs, the overhead (indirect costs) offers more opportunities to innovate. Nevertheless firms such as ARCADIS are always aiming to provide their solutions against the lowest costs. And thus the topic of overhead cost reductions is daily business. Each change inevitably comes with risks. These risks can be either internal or external of nature. These risks are essential to take into count during the revenue model innovation process. Not only risks will be faced during this change in revenue model. There will be some hurdles that need to be taken. These hurdles are better known as barriers and these barriers are of internal and external nature. Both the risks and barriers are therefore taken into count in the revenue model framework. It can be concluded that barriers such as threshold limits and regulations, corporate culture and risk adversity, country factors (language and culture) and a firms strategy, influence the successful implementation of revenue models. If firms are able to take these hurdles effectively many opportunities lay ahead. The resistance against a change can be expected from both the market and the own employees. Therefore a certain level of managerial support is needed to align the innovations with the company strategy. Moreover the consultants need to develop relationships with clients, in order to gain trust and provide them with insights on the benefits of revenue model innovation. This last remark is a difficult one. Due to the nature of the clients, their thoughts on projects and the costs associated with the projects differ. Private firms are currently more open for the usage of other revenue models than fixed price and hourly fees. Therefore this group of client offers the most opportunities to do so. Nevertheless the majority of clients of consultancy firms are public firms. Therefore the usage of other revenue models needs to be stimulated and the public market should be educated what the benefits of revenue model innovations are for their projects (read: what the benefits in terms of costs are). So revenue model innovation offers opportunities to secure market share and growth for strategic consultancy firms in their international environment. To do this effectively, these previous mentioned factors need to be carefully considered. If the focus is only on the revenue model this is not the solution. The total offer combined with these revenue models need to be aligned, to come up with the best solution for both the client and the consultant. 8

9 Preface / Acknowledgements The last deliverable before receiving the Master of Science in Innovation Management title is a master thesis project report. After more than three years of pleasure, having a job and of course studying hard this was the last hurdle to take. Not only ARCADIS is broadening their scope of interest, so did I. After finishing my bachelor degree Automotive Engineering it was time to learn some managerial skills. Innovation Management at the TU/e was, and still is the best choice I have ever made. Together with my classmates I had a lot of fun during the hours we have spent working on the several topics. Besides this fun we have learned a lot from each other, for example how to work in groups, how to divide the work, etc. Furthermore we have learned (how) to be critical on each other s work to improve the final outcomes. My personal interest was triggered by some topics like Marketing and Innovation, Service Engineering, Strategy and Technology Entrepreneurship and New Media. Although the last topic will not be covered in the research project, I think it is an interesting medium to reach (potential) customers. Started on the 10th of November 2012 this master thesis project is finished within 21 weeks. This document presents the outcomes of the master thesis project at ARCADIS Netherlands Division Water, Market group Delta s and Rivers, advisory Group Strategy and Decision making (S&B), (see Appendix I). Before the reader starts I would like to thank my supervisor in ARCADIS Dhr. Marius Kiers and sponsor Mrs. Ursula Blom for offering me the opportunity to do a project at ARCADIS. Furthermore I would like to thank all other colleagues for their input and support. I appreciate the time Dr Umut Konuş and Dr. Jeroen Schepers are spending, and are willing to spend to be the master thesis supervisors. Finally I would like to thank my family, my parents for their support, which made me able to do a Master. And of course my girlfriend who was my motivator to finish the project, and who supported me during the hours I was working on this project. For me remains nothing more than to wish you a pleasant reading. Ernst Vossers 9

10 1. Introduction The goal of this section is to elaborate the context in which the research takes place, and what the drivers or motivations are. In order to do so, both sections 1.1 and 1.2 explain the inducements for the research. Section 1.3 clarifies the definitions used during the research and section 1.4 identifies the problem definition. Finally section 1.5 elaborates the structure of this report Inducement for the research Services are becoming more important by the day and a shift from manufacturing to services is evident in many Western economies (Cicic et al., 1999). Services have grown to almost 75 percent of the GDP (Gross Domestic Product) in higher income countries, such as the Netherlands (Francois and Hoekman, 2009). Professional Service Firms (PSF s) and their internationalization process receive particular attention in research during the last decade. PSF s that are securing revenues by internationalization is very common nowadays, this is a result of the world wide globalization (Stumpf et al., 2002) and innovation performances, (Cainelli, et al., 2006). A special group of PSF s are the (strategic) consultancy firms. These firms are also broadening their scope of interest by providing their services across their national borders. The generalisability of current research findings for service firms is limited. Javalgi et al., (2003) support this finding that the amount of empirical research of internationalization of service firms is low. Moreover Deprey and Lloyd-Reason (2009) stated in their research that all the previous work was sector specific, focused on small and medium firms, and that none of these previous studies pertain directly to (strategic) consultancy firms. This leaves us with an understudied topic in current literature. The organic growth at ARCADIS (a large environmental consultancy and engineering company) is concerning the management at ARCADIS. To prevent ARCADIS from stagnation, an internationalization project is thought to be a good opportunity to secure revenues. Not only ARCADIS is facing difficulties in their organic growth. (Strategic) Consultancy firms like McKinsey, The Boston Consultancy Group and Roland Berger are struggling in this competitive environment. In general, there are four pressures that indicate the difficulties for these firms. First the economic conditions (recession) have forced (strategic) consultancy firms to reevaluate their current business model(s). Their clients are demanding higher flexibility in pricing of the consultants' advice. Secondly, the consulting services tend to be seen as overpriced and suspected for not always delivering the expected value. As a result, their current (often traditional) revenue model is outdated. Third, (strategic) consultants are forced to track the internal performance and the work they provide. This implies working more efficient, effective and delivering higher quality in a shorter period of time. Finally, in order to deliver this higher quality work internal pressure arises for the management to develop or hire more experienced experts. The positive side of this is the significant amount of hands-on knowledge, as they are able to generate well and operationally straight-forward advice in the shortest period of time. The negative side of this is that these experts are more costly, and leverage logic of the firms is disturbed. This leverage logic is very common and very important for these firms. 10

.")

11 In contrast what people might expect, the economic crisis also offers opportunities. In the Marketing Tribune Colum of Joris van Zoelen it is stated that every organization will face a few crises during their life. These crises force firms to reevaluate their current situation and strategies. The topic of revenue models is underexposed, and thus requires more attention. Firms can stay one step ahead of the competition if opportunities are carefully considered and converted into goals. These goals need to include potential solutions to overcome the previous mentioned pressures. One of them might be changing the revenue model with its corresponding business model (Osterwalder and Pigneur, 2010). Both consultants and a majority of their existing clients are thought to be thinking traditional, so a good moment to introduce these changed models is during the internationalization of their professional services. Internationalization (Ruigrok and Wagner, 2003, and Hitt et al., 2006a), international diversification (Hit et al., 2006b, and Capar and Kotabe, 2003), international expansion (Contractor et al., 2003), and (Sarkar et al., 1999)), globalization and multi nationality (Sullivan, 1994) are topics of recent research focusing on the same strategic management issue. The two most used terms, 1) international diversification, is explained as a strategy through which firms expand their sales of goods and or services across the borders of global regions and into different geographical locations or markets (Hit et al., 2006b), and (Capar and Kotabe, 2003). 2) Internationalization refers to the process in which a firm gradually increases their international involvement (Johanson and Vahlane, 1977). The clients and or services provided are new, thus a changed revenue model is more likely to succeed. The combination of the topics: international oriented strategic consultancy firms and revenue model innovation (business model innovation) are not found in the literature. To fill this theoretical gap the project at ARCADIS will be used to provide both practical and theoretical support. This means that this study will try to solve a gap in the literature as well as improve the process at ARCADIS Personal Inducement for the research My personal interest focuses on service development. An important aspect of service development is the selection and usage of the appropriate business model. My personal interest is further triggered by the revenue model that is a part of the business model. This topic receives not only on the University attention, but the market is also innovating. Well respected researches as for example Chesbrough, Osterwalder and Pigneur, and Amit and Zott have been previously researching this topic. One of the topics that is understudied are the new types of contracts and thus sources of revenue. These are of high importance in the current turbulent environment. The master thesis project is supposed to provide the scientific world with new or changed findings that are not yet elaborated. Secondly ARCADIS is willing to provide me with the practical insights on this issue. ARCADIS is also dealing with issues caused by the crisis and the competitive environment. Furthermore ARCADIS is interested in the international aspect of these developments Definitions This section explains the key definitions used in the research, in order to develop a clear understanding of the research and the parameters. First the definitions of PSF s and strategic 11

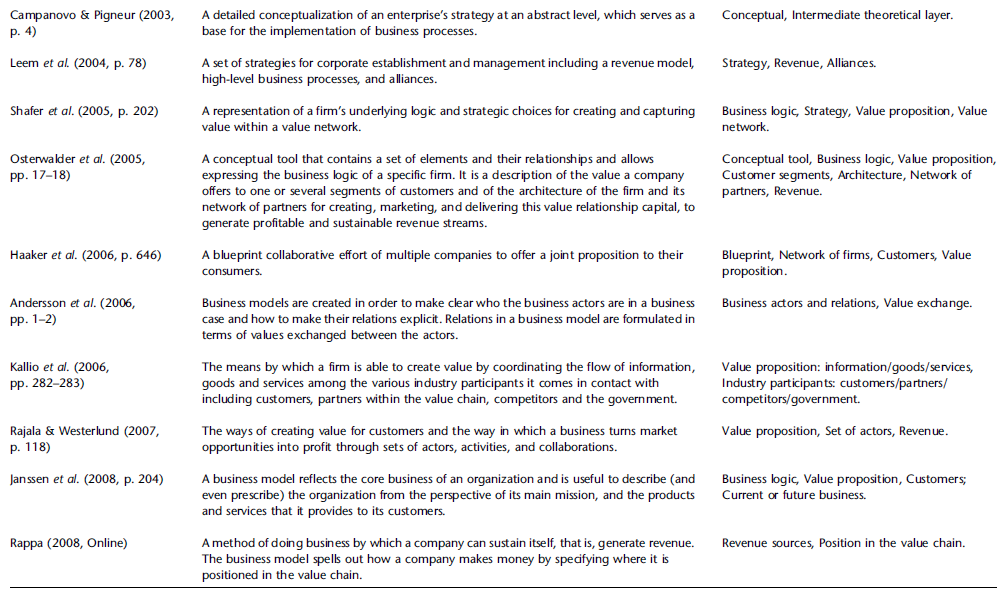

12 consultancy are explained. Followed by the definitions of a business model and business model innovation. Finally the concept of the international environment is explained. Professional Service Firms Kaiser and Ringsletter (2011) explain the definition as follows: Professional Services Firms (PSF s) are firms like; consultancies, auditing firms etc. These firms provide their clients with services based on the knowledge available in the firm. This knowledge comes from skilled and independent contractors or consultants whose occupation is the rendering of such services. The critical success factors for these firms are the knowledge, the relational competence and the reputation. Furthermore it is argued that service characteristics create a context in which the consultant has to convince the client that consultants have something of value to offer (Lu, and Beamish, 2004). Strategic Consultancy There are many different areas in which consultants are active. One could think of strategy, human resources, internet, process public relations, performance, and engineering. In all these different areas the consultants are providing the client with advice or information on the topic of interest for their projects. These projects can be divided according to Kaiser and Ringsletter (2011) into three categories, namely: brain, gray hair and procedure projects. The Brain projects are usually executed when the client is dealing with problems which are of strategic importance for the client. The client does not have the knowledge in-house to solve the problem, thus external knowledge of the consultant is needed. The nature of these projects is quite different. For sake of this research ARCADIS, and its subsidiaries (see Appendix I) and competitors such as RoyalHaskoningDHV, Twynstra & Gudde are regarded as a strategic consultancy firm because they provide their clients with strategic advice for environmental issues. The topics for these environmental advises are really broad, just as the clients; from SME s (Small Medium Enterprises) and local governments to MNE (Multi National Enterprises)/MNC (Multi National Clients) and the EU (European Union). The department S&B (strategy and policy making) is a good example of a department within ARCADIS providing these services. Business Model (innovation) Business Model (innovation) is one of the hottest topics in current business research. The concept of a business model is explained in various ways; see Appendix III for an overview. This research will use the concepts for Business Models and Business model Innovation of: Amit and Zott (2010), Osterwalder and Pigneur (2010). Osterwalder and Pigneur (2010) described the business model as the rationale of how an organization creates, delivers, and captures value. For the explanation of the components of a business model the Business Model Canvas (BMC) of Osterwalder and Pigneur (2010) is used (see Appendix IV). Business model innovation occurs when a firm adopts a novel approach to commercializing its underlying assets (Gambardella, and McGahan, 2010). This innovation leads to a change in one of the 9 building blocks of the BMC (see Appendix IV ). According to Amit and Zott (2010) business model innovation consist of adding new activities, linking activities in novel ways or changing which firms performs an activity. 12

13 Revenue Model Innovation: In contrast to business model innovation, revenue model innovation is an understudied topic in current research. The combination of the building blocks cost structure and revenue streams of the BMC are representing the revenue model (see Figure 11). The changes in the current revenue model in this context will be further described as revenue model innovation. The term innovation in this context requires some further explanation. Innovation is conventionally referred in the marketing literature as a technology breakthrough. In this research innovation will described as a pervasive attitude that allows businesses to see beyond the present and create a future vision (Kuczmarski, 1996). This future vision is needed for the development of new customers value. This can be done through solutions that meet inarticulate, new and or change (market) needs in value adding new ways. International Environment Finding markets for products is not bounded within the home countries border. Firms are actively seeking markets across the borders (market expansion), introducing new services in well-known markets (product expansion), or introducing something completely new in a new market (diversification). Recent research has been done on: international diversification, international expansion or internationalization. Because of the nature of these terms they will be used interchangeably throughout this research. Research of Johanson and Vahlane (1977) identified that internationalization of a firm is a process in which the firm gradually increase their international involvement. The international environment for this research is bounded within Europe. Furthermore the Netherlands is regarded as home country for ARCADIS (based on the history and the location of the headquarters) Problem definition In the current turbulent economic environment many western consultancy companies, such as ARCADIS, are facing slowing organic growth perspectives. ARCADIS is one of the top 3 professional service providers that focus on global environmental engineering and consultancy. To stay in the top 3, ARCADIS must stay one step ahead of the competition. Within this environment providing (high) quality services is not good enough anymore. Innovation and a new ways of earning money is necessary, otherwise the fall of ARCADIS is near (Robert Kroon, ARCADIS, 2012). This view is not a unique idea. Moore (2008) states that innovation and continual adaptation is essential for the survival of organizations. This idea is not developed in the last years. Early research of Kash (1989) introduced the concept The new World of Competition Based on the literature gap, the four premises combined with the problems and opportunities of ARCADIS have been translated into the following problem definition: It is unknown how innovation of business models (with innovated revenue models) during internationalization can be used to strengthen ARCADIS top 10 position (see Appendix I, Figure 10) as a global strategic consultancy firm. Furthermore it is unknown if (new) clients are accepting a change in the revenue model for new or existing services of ARCADIS. This problem is translated into a research objective with corresponding research questions. These questions will be explained in the next sections. 13

14 Research objective The project consists of two sub projects (parts), a scientific and a practical part which are related to each other. The scientific part will focus on the theoretical applicability of the results. Combining the findings from the literature with practical findings from case studies and interviews will result in a scientific explanation of the research question. In the next section both the theoretical and practical relevance are elaborated. In order to fill the gap in the current literature, and providing ARCADIS with managerial insights for the current problem, this project is started. Further, the practical part will provide insights from the market by interviewing several experts in this field. The information of both will be used to develop a comprehensive and unifying model to successfully change the revenue model (as part of the business model) for strategic consultancy. Several questions are raised: What needs to be changed in the revenue model in order to become successful in this environment? Is it possible to change the revenue model of strategic consultants? What needs to be changed in the revenue model to become successful? The different steps (see Figure 1) before the actual start of the research are as follows: Step 1, my personal interest combined with the challenges of ARCADIS has triggered my attention for different topics. A logical consequence of this is that the literature review is done on the topics, to gain more scientific knowledge. Step 2, the actual literature review is conducted. The topics of this review are: internationalization, business model innovation, and strategic consultancy. Only studying these topics did not identify a gap, (see chapter 5, Theoretical Relevance). So step 3 the orientation interviews are conducted. These 6 interviews have shown that there is a need for strategic consultancy firms to start changing their revenue model/ earnings model, (see chapter practical relevance). By combining both step 2 and step, the gap in the literature is explained (see chapter 2.4). This gap has shown the necessity to start elaborating the main research topic (and question). Based on this, the research (sub) questions are derived. Figure 1 Research objective Main research question As explained in the problem definition the usage of revenue model innovation is currently understudied. In order to propose a solution for this problem the following main research question is elaborated: What changes in the revenue model (as part of the business model described with use of the theory Osterwalder and Pigneur (2010)) need to be made in order to be successful as strategic consultant in an international environment? 14

15 To answer this question the previous mentioned definitions will be used. The main research question is further divided into some sub questions. These sub questions are elaborated in the next section Research questions A theoretical framework is developed in order to gain insights in the usage of revenue model innovation by strategic consultants in an international environment. As been elaborated the research questions address the different topics. Each of these topics is explained in research with use of several theories. Theories that are applicable for the situations will be included in the research. These theories will be further used to develop the comprehensive and unified framework. The following sub questions are derived: 1) Which internal and external changes are necessary for the revenue model in the cost structure (Q1A), and the sources of (Q1B)? This question is answered as follows: First a clarification of the revenue models currently used by strategic consultancy firms, such as ARCADIS, are given. Thereafter an elaboration is given how these firms use these or other models in the international environment. In order be successful it is essential to stay one step ahead of the competition. Trends and developments from revenue models in the Netherlands form the basis for this. These developments are elaborated and will also provide me with suggestions for changes. Each change inevitably comes with risks. So the next sub question is: 2) Are there potential internal and external risks associated with these changes, and if so what are those? This question will be answered as follows: What are the risks for the firm to start using new revenue models? Is there a risk of cannibalization of their products? Are they becoming competitors of their own OPCO s (operating companies)? Are these revenue models hard to copy, and do they involve more risk taking activities of the firm itself? All of these factors might hinder the change of revenue models of the firm, and thus need to be incorporated. Not only risks will be faced during this change in revenue model. There will be some hurdles that need to be taken. These hurdles are better known as barriers. These barriers are of internal and external nature and will be elaborated. So the last sub question is: 3) What internal and external barriers will hinder the successful implementation of these revenue model innovation(s)? Business model innovation and internationalization both need to deal with barriers. As the revenue model is a part of the business model, there are also barriers. The revenue model innovation takes place in the international environment, and thus the barriers for internationalization will also hinder this change. This question will be answered as follows. First the internal barriers and their impact on the revenue model are explained, followed by the external barriers that are hindering revenue model innovation. Both will be incorporated in the final comprehensive and unifying model. 15

16 Relevance The relevance of this project is twofold, namely practical and theoretical. In this section both the practical and theoretical relevance for the research will be explained Theoretical relevance Based on the previous conducted literature review it can be concluded that the topics of internationalization, business models and business model innovation are hot. Some wellknown and respected researchers are developing new models and theories about these topics. Chesbrough (2007) states that companies have a business model innovation leadership gap. Furthermore Chesbrough (2010) explains business model innovation with opportunities and barriers. There are two drivers for this research. The first is based on the research of Kujala et al. (2010). Kujala et al. (2010) states that further research should be conducted to determine the contextual factors or the drivers and barriers that affect the choice of the business model in project-based firms. The second is based on Deprey and Lloyd-Reason (2009), who stated in their research that all the previous work on internationalization of PSF s was sector specific, focused on small and medium firms, and that none of these previous studies pertain directly to (strategic) consultancy firms. Furthermore the model of Patrick Stähler, (see Figure 12) has triggered my attention. This model builds up on the previous model of Osterwalder and Pingeur (2010). Stähler added the culture and value blocks to the model. In these blocks leadership style, relationship style and values are included. These three points are of particular interest for strategic consultancy firms in their relationship with their clients. As has been elaborated previously the following topics received my attention. 1) Internationalization or international diversification as a strategic development option to secure market share and profits. 2) The usage of innovative business model (and their underlying revenue model), and the rationale behind business model innovation. 3) The topic of consultancy, and the characteristics of these types of services. These topics are addressed in several researches, for example: Appelbaum and Steed 2005, Osterwalder and Pigneur 2010, and Chesbrough The literature review is used as input for 6 orientation interviews. These interviews combined with the fields of interest have been directing the research (see section practical relevance). With use of the interviews and the literature review I identified a gap. This gap shows there is relevance to study this topic further. Practical relevance It has become clear that ARCADIS might be facing difficulties and opportunities in their current environment. This section will indicate the practical relevance (and thus opportunities) to start with an internationalization process at ARCADIS Netherlands. This relevance will be supported by examples from the six interviews conducted before the start of this project. As globalization increases, so does the attention paid to the internationalization of Dutch companies. The appearance of new players on the (European) market means on the one hand 16

states that companies have a business model innovation leadership gap. Furthermore Chesbrough (2010) explains business model innovation with opportunities and barriers.")

17 that Dutch companies are being confronted with greater (foreign) competition on their domestic market. On the other hand, the same circumstances also create more opportunities on foreign markets. Not only strategic consultancy firms such as ARCADIS are focusing on expanding their market to foreign countries. In a letter ( Buitenlandse markten, Nederlandse kansen (2011)) to the House of Representatives, (currently ex) Minister Verhagen emphasizes the need for companies to expand their foreign market involvement. This further internationalization is necessary for a prosperous, sustainable and entrepreneurial Netherland. More recently the Dutch House of Representatives identified several topsectors in the Netherlands of which water is an important sector. The Netherlands is known as Waterland, our source of growth and prosperity. With the innovation contract, Nederland Waterland the ambitions for the topsector are emphasized and the responsibility for further expansion throughout the world are shown. One of the targets is to double the industry by 2020, in order to show the Dutch identity and power to innovate (Ministry of Economic affairs, 2012). The share of services in total Dutch exports remained approximately 20 percent (CBS, 2010). The first two quarters of 2012 indicated growth revenues of PSF s, but the expectations are not as good as before. PSF s are facing these unexpected challenges today (Stumpf et al. 2002). The conjunctuurenquête van July 2012 of the CBS indicated a trend in which 18% of the PSF s are expecting a negative economic climate. In order to prevent PSF s from (further) stagnation, internationalization is a potential solution. Internationalization deals with expanding their offerings and office locations in response to the changing situations more comprehensive and integrated services are a potential solution (Stumpf et al. 2002). There are four important motives to start operating in a foreign country: Securing the market share, and thus profit in order to reach the targets (supported by Marjolein Van Wijngaarden, Ursula Blom and Harm Albert Zanting, ARCADIS 2012) Securing the organic growth, (supported by Ursula Blom and Harm Albert Zanting, ARCADIS 2012) Attracting the right human resources, (supported by Harm Albert Zanting, ARCADIS 2012) Supporting key clients across the national borders, (supported by Marjolein Van Wijngaarden, ARCADIS, 2012). Reihlen et al. (2009) provides some examples of PSF s that were engaged in moving advisory activities (services) across borders. Accounting firms such as Deloitte and Haskins Sells or Price Waterhouse have followed their industrial clients since the late 19th century to the United States (Aharoni, 1999). Moreover Reihlen et al., (2009) explains the internationalization process of Deutsche Treuhand-Gesellschaft (DTG, a KPMG company). DTG was not only a particular relevant case for the study of Reihlen et al., (2009), but today as part of KPMG, it is one of the top 4 largest international accountancy/ advisory firms worldwide and is the only Big 4 accounting/ advisory firm with an European origin. Reihlen et al., (2009) identifies that PSF s are able to create a significant part of their competitive advantage by defining a competitive strategy as a direct result of their foreignbased activities. The purpose of this competitive strategy is to achieve sustainable competitive advantage and thereby enhance the business's performance (Bharadway et al., 1993). 17

18 The 6 orientation interviews identified the need to further study the internationalization strategy of ARCADIS. The public market in the Netherlands is saturated. The Dutch market doesn t offer many opportunities anymore. The competition is increasing, and appears from unexpected competitors (Marjolein van Wijngaarden, ARCADIS, 2012). There are lots of opportunities outside the national borders (Harm Albert Zanting, ARCADIS, 2012). To be successful, a sound (Ursula Blom, ARCADIS, 2012), and a throughout the firm supported (Harm Albert Zanting, ARCADIS, 2012) internationalization strategy is necessary. A part of this strategy is the innovation of business models, and their underlying revenue model. Only focusing on providing high(er) end value services with potential better margins isn t the best solution. Extending the service range will improve the profits of ARCADIS. The revenue model of consultants is becoming outdated. The prices cannot be increased, but the services need to be extended (Marjolein van Wijngaarden, ARCADIS, 2012). That the topic of revenue model innovation is hot is supported with the report of Agentschap NL (2012) (De waarde van nieuwe verdienmodellen). The report provides findings of innovations on value creating with use of revenue model innovations in urban delta developments. This is one of the markets ARCADIS is proving it s strategic services for Report Outline In order to guide this study the reflective cycle by van Aken et al., (2007) is used. This document is structured as follows. In section 2 an elaboration is presented on how the research is conducted. This includes the methodology used, the data collection and analysis procedure. Thereafter the quality issues regarding the used methods. Chapter 3, the theoretical background provides a literature overview of the topics that will be addressed in the research. Followed by chapter 4 that provides the information gathered from the field research. Further the analysis of the results and the final general and comprehensive model (framework) are elaborated. Chapter 5 will answer the questions as proposed in section 1. Further the conclusions and limitations are elaborated. The appendixes starting after the reference list can be used to gain more insights in this project. The appendixes are readable without background knowledge, but with use of the information throughout this proposal the relevance becomes clear. 18

, and a throughout the firm supported (Harm Albert Zanting, ARCADIS, 2012) internationalization strategy is necessary.")

19 2. Research Methodology After elaborating the problem definition, research objectives and their corresponding research questions the research methodology is elaborated. This section will provide a framework for the guidance of the researcher to ensure the quality of the deliverables. The main question discussed in this chapter is: Which steps need to be taken during the research to ensure this delivery? The regulative model cycle of Van Strien (1986) that is following the business problem solving approach, describes the knowledge (internationalization, business model innovation) deducted from literature which is used to improve the current situation of strategic consultants, such as due to the stagnating growth of ARCADIS. Furthermore the reflective model cycle of Van Aken et al., (2007) reflects how the integration between a proposed solution and the current situation works, as shown in Figure 2. According to van Aken et al., (2007) projects related to business problem solving can be divided into three phases: design, change and learning. These phases consist of the following five chronological steps: 1) Problem definition, 2) Diagnosis, 3) Design, 4) Intervention and 5) Evaluation. The reflective cycle by Van Aken et al., (2007), as shown in Figure 2, will be used to ensure the academic quality and outcome(s) of this project. This research is divided into a practical part and a theoretical part. The practical part concerns a set of explorative qualitative in-depth interviews. As van Aken et al., (2007) describes, the qualitative research is conducted when qualities of things should be assessed. The explorative nature of this research is identifying the factors influencing the success of revenue models in the given context. The theoretical part of this research, the literature review, which is also explorative qualitative of nature is providing insights in topic of business and revenue models (innovation) in the international context for strategic consultants Research classification Verschuren en Doorewaard (2005) explain the difference between practical and theoretical research. Both are applicable for this research, but the main focus is on the theoretical research, because this research aims to provide theoretical scientifically insights. Verschuren en Doorewaard (2005) further explain the difference between theory development and theory review. This research focuses on theory development. A smaller part of this research includes a review of the proposed solutions, but not the theory itself will be reviewed Research strategy The selection of the appropriate research strategy is the most important decision, this further influences the whole research. The research has an explorative problem definition, so unstructured qualitative research is preferred (Van Der Velde et al., 2000). The usage of quantitative research is not appropriate because of this explorative nature. Furthermore the Analysis Evaluation Intervention Other Input Reflection Reflective Cycle Regulative Cycle Plan Figure 2 Reflective cycle Documentation Problem Definition Diagnosis 19

that is following the business problem solving approach, describes the knowledge (internationalization, business model innovation) deducted from")

20 absence of scientifically explanations on the topics is another reason to do quantitative research. A drawback of this type of unstructured research is the fact that it takes more time to gather qualitative data, although these insights are often regarded as really valuable. Qualitative research targets at developing an understanding and insights gathered with use of observation, interviews, ethnographic fieldwork, discourse analysis or textual analysis based on small samples on the topic of the research. The researcher is interpreting and reporting verbal and contemplative the findings (Verschuren en Doorewaard 2005). The theoretical part describes literature related to the topics, and will be assessed on the relevance and quality before it is included. The literature review provides the research with secondary data, which will be combined with the primary data gathered by interviews to support the findings (Blumberg et al., 2005). These interviews are one of the different types of case studies. CSR (Case Study Research) is appropriate for this project, because it focuses on describing, understanding, predicting and/or controlling: process, organizations, groups, industries, cultures, or nationality that allows us to perform in-depth investigation (Fellows and Liu, 1997) to gain insight why and how to design a solution for ARCADIS and comparative firms (Woodside & Wilson 2003, Yin 2009, Blumberg et al., 2005). The results of the CSR will be used to support the general (framework) model. Each research strategy and methodology has benefits and drawbacks, so it is essential to assess the data on the quality. First the unit of analysis is further explained in the next section Unit of analysis Before suggesting a set of criteria for judging the project, (an) appropriate selection unit(s) of analysis is determined (Shrivastava, 1997). In the most ideal project, the unit of analysis is an existing theory in the research field. According to Shrivastava (1997) a research project delineates the content domain that is the focus of the research. This focus implies that a set of questions of interest and a set of research methods are determined for the project. A sound research is supported by a set of underlying theoretical findings from the literature. The units of analysis in this project are strategic consultancy firms. As this study will be a qualitative study, this section will explain the used sources to collect the data. An overview of the used sources will be given in the next sections Part 1 Literature review A literature review is conducted before the final thesis question development, see Step 2 of Figure 1. After the elaboration of the problem definition and the corresponding research questions a more extensive literature review is conducted. Different types of literature are used during the project, scientific and some popular nonscientific materials. The literature is reviewed as follows: First the most relevant literature is reviewed. From this relevant literature the references are scanned and reviewed if these were relevant to gather new insights, finding new keywords and elaborating new terms. After a few rounds a state of theoretical and empirical saturation is reached. This saturation point implies that reviewing more literature doesn t add any new and significant insights to the research (Yin, 2009). A 20

.")

21 great advantage of (scientific) literature as a source is that it adds various insights from different fields that can be used as theoretical explanations of the research questions Part 2, Case study There are several reasons why case study research is suitable for this research: 1) The main research question and the sub questions are suitable for case study research, due to nature of the what, why and how (Yin 2009) questions that are used for explanation. The main research question: What changes in the revenue model (as part of the business model described with use of the theory Osterwalder and Pigneur (2010)) need to be made in order to be successful as strategic consultant in an international environment? describes the changes needed for this situation. The sub questions are further identifying barriers and risks for these thought to be successful changes. 2) Yin (2009) explains that CSR is more suitable when the phenomenon cannot be completely isolated and tested with experiments. The factors influencing this phenomenon cannot be isolated and explained systematic and directly. 3) Case studies are used aims to explain the current situation, and not the historical situation. Based on the reasoning of Yin (2009), case study research is an empirical research whereby the current situation is explained when the context and boundaries are not clear, and there are multiple sources of evidence used. Based on Yin (2009) the best way to answer the main research question and give a clarification for the problem definition is to use an explorative qualitative research that will make use of multiple case studies. Further to ensure external validity, multiple case studies are preferred (Yin 2009). Multiple case studies are useful because the goal of the research is to develop a general framework with a set of thought to be relevant variables. Moreover multiple case studies are preferred above a single case study, because the lack of precious found empirical data/ cases that are: 1) crucial 2) typical or representative, 3) long lasting, 4) sensational or revealing, and 5) unique or extreme (Yin 2009) Selection of the cases Before the selection of case studies can be made, an accurate elaboration of the case itself must be made. The unit of analysis, as previous explained, is not a single person or an organization. Unfortunately some researchers make a mistake by selecting a single person or a single organization (Gomm et al., 2000). In this research it is not ARCADIS that is the case, but the strategic consultancy firms, such as ARCADIS. The interviews conducted are not bounded within ARCADIS, or within a specific division of ARCADIS. Other Firms like NPC (RoyalHaskoningDHV), Syntens and The Bridge are also included in the research. The selection of interviewees is done by accidental sampling (Powel, 1997). Accidental sampling is also known as grab, convenience or opportunity sampling. This type of sampling is a nonprobability sampling method, which involves the sample of interviewees being drawn from that part of the population which is close to hand, in my own network. The population can be regarded as readily available and convenient. The interviews are taken in a face to face setting 21

22 in the Netherlands, and with use of communication tools outside the Netherlands. A drawback of this methodology is that the results cannot be generalized scientifically. The total population might differ too much from the taken sample, and thus this would not be representative enough. Several important considerations for researchers using convenience samples include (Powel, 1997): 1) Are there controls within the research design or experiment which can serve to lessen the impact of a non-random convenience sample, thereby ensuring the results will be more representative of the population? 2) Is there good reason to believe that a particular convenience sample would or should respond or behave differently than a random sample from the same population? 3) Is the question being asked by the research one that can adequately be answered using a convenience sample? Data collection Choosing between the data collection methods (documents, archival records, interviews, direct observation, participant observation, and artifacts (Rowely, 2002)) depends on the type of data best illuminates the research topic on practical considerations (Patton 2002). The data gathered with these methods can be divided into primary and secondary data. In this research both types of data will be used in this research. The primary data is gathered by in-depth interviewing. This information will form the basis of this research, and will be combined with secondary data that is gathered from journals, books, internet, brochures, presentations, annual reports, and some other interesting sources. By using multiple sources of evidence, and research methodologies the triangulation will be improved (Golafshani, 2003). The considerations to use a certain type of data depends on 1) if the data already exist, 2 ) the nature of data, 3) the subject matter and the study population (Ritchie et al., 2003). There is some information available on the individual topics of this research. This data is therefore regarded to be secondary data (part 1 of this research). This primary data (Part 2 of this research) is found by the researcher himself, and can be directly linked to the actual research objective. There are five key features that are in favor of using in-depth interviewing in this research above other methods (Legard et al.,2003). First, in-depth interviewing allows more flexibility than other methods Secondly this method allows interaction between researcher and interviewee. Thirdly, the researcher can ask why and how questions to elaborate topics of interest deeper. Fourthly, new knowledge and insights can be created because of the interactions and the deeper elaboration. Finally, in-depth interviewing is done in a face to face setting. Interviewing by phone is not supportive for the method. Because of the four previous mentioned features combined with the interpretation of the researcher when he/she is not present (read: in a face to face setting, or by video conferencing) during the interview. Focus groups offer another opportunity to gather primary data, nevertheless based on the following explanations of these issues in depth interviewing is preferred above focus groups. Revenue model innovation of strategic consultants is an understudied topic. Therefore elaborating this linkage is a new research topic. Questions such as: What are motivations of 22

23 both clients and consultants to use these model, etc? are raised. The employees of ARCADIS are located at several offices, that are easy accessible for me as researcher. The other interviewees are located near the TU/e and the offices of ARCADIS. All the interviewees have a full agenda, therefore visiting them on their site was required to gather the information. The topic of revenue model is investigated by the researcher in detail. Involving creativity to come up with new models is not required. It is preferred for identification of barriers, risks and opportunities to use different insights of the problems Interviews The in- depth interviewing methodology, conducted by employees of ARCADIS, experts from the fields and with employees of competitors is used to gather (a wide diversity of) information or knowledge on the topic of interest. This information is relatively easy accessible, and can be gathered in a short period of time. Patton (1987) suggests three basic approaches (based how structured they are) to conduct qualitative interviews, namely: 1) informal and conversational, 2) a general interview with a guided approach, 3) standardized, open-ended interview. The more structured the interview, the less room for natural interaction between researcher and interviewee. A general interview, also known as semi structured, is the most suitable for this research. By developing a set of questions the topics of interest will be covered, but the depth of the questions depends on the interaction between researcher and the interviewee. The interview will be held in the following languages: English or Dutch. After the interview the interviewee received a short summary for confirmation of the findings. After the conformation that the gathered data is correct, the data is suitable to be analyzed. In Appendix V a list of the interviewees is presented. In the next section the rationale of this selection is explained. Rationale The rationale behind the selection of the interviewees within ARCADIS is the following: All the employees are regarded as senior consultant, or have been promoted to a (senior) management position. Therefore these employees are not new to the market and thus have enough knowledge on these topics. All these field experts have affinity with strategic consultancy and/or business model innovation and/or internationalization. By selecting the managers and consultants with different functions inside of the firm, the possible findings will have a wide support throughout the several departments of ARCADIS. Managers have different views of the market compared to their subordinates. By incorporating the opinions of several managers, with different positions within the firm, the generalizability is enhanced. Furthermore managers are selected both within and outside of ARCADIS. This makes the findings generalizable outside of ARCADIS. The director(s) and the employees of the business development department are, as the department name already suggest, working on developing (new) services. Their focus is on using new types of contracts, finding new markets, finding new customers and developing new alliances for each of these topics. Further their knowledge of the market is broad, which is useful to identify trends. 23

24 Data analysis As elaborated, several methods of gathering data/information will be used. This information is further analyzed and translated into concrete findings and recommendations. The concepts found in the secondary data (literature) are used for the interpretation of the primary data (interviews). The primary data is analyzed by making use of content analysis. This method is summarizing a quantitative analysis of the findings that rely on a scientific method. Further this method is not limited to the types of variables that may be measured, or the context in which the messages are created or presented. This method includes taking attention to objectivity, inter-subjectivity, a priori design, reliability, validity, generalizability, reproducibility and hypothesis testing. Interpreting and analyzing data in research comes with the following epistemological assumptions Travers (2001) even when they are not aware of it: Positivism, interpretivism and positivism realism. Furthermore the rigor relevance debate of Shrivastava (1997) is one of the concerns for the case study. Rigor refers to the question whether the research is well grounded in existing theories, in contrast to relevance that refers to the usefulness of a research outcomes project for managers. The criteria of Shrivastava (1997) for assessing the rigorousness of a research project are taken into count as follows; First the conceptual adequacy, that is taken into count with the literature review, measure the extent to which a research project applies the knowledge of its base disciplines to create an adequate conceptual framework. Secondly, methodological rigor focuses on the research methods used. Because of subjective methods used the researcher needs to deal with qualitative data, interpretive data analysis and intuitive inferences (Morgan and Smircich, 1980). Shrivastava (1987) discusses that it is possible to evaluate these techniques on a subjective-objective continuum. Therefore the usage of multiple sources of data in this project ensures that the used methods give different (supporting) views of the problem statement and the potential solution(s). The third rigor criterion of Shrivastava (1987) is the extent of accumulated empirical evidence supporting the theory used in this project. In this project a case study will be conducted, and according to Yin (2009) case studies can be regarded as a threat to empirical evidence. The case study focuses on the impact of revenue models on the internationalization process of strategic consultancy firms. The evidence found will be compared with previous comparable research to be able to generalize the findings. The theories used on the earlier mentioned topic are all proved by scientific literature. The relevance criteria of Shrivastava (1987) will be ensured as follows. The work should be meaningful and the goal must be relevant, that is ensured with the fact that the project is initiated and conducted by ARCADIS. The operational validity will be taken into count by designing a theoretical model for revenue/business model innovation. Innovativeness focuses on the added value by providing non-obvious and new insights into the practical problem revenue/business model innovation by strategic consultants in an international environment. The actual implementation, and the cost acquiring with this are out of scope. 24

25 2.6. Research quality Research comes with assumptions, and these assumptions always imply a debate on the quality and generalizability of the findings. According to Yin (2009) case study research needs to deal with four types of criteria to assess the quality of the research: reliability and three types of validity (construct, internal and external). Reliability The reliability of the results in this research are regarded as reliable when they are independent of the particular characteristics and can therefore be replicated in other studies (Van Aken et al., 2007). According to van Aken et al., (2007) reliability of interviews can be influenced by four different variables: the researcher, the measurement instruments, the situation and the respondents. In order to prevent this research from non reliable results the interviews are standardized. Therefore explicit procedures for data collection, followed by the analysis and the interpretation are used. The semi structured interview method, that is used, is suitable for this, because the answers are given in a format which can be evaluated. Triangulation (Golafshani, 2003) is used to further improve the validity and reliability of research or evaluation of the results. This strengthens a study by combining different research methods that differ in type of data, or in the combination of research methodology. In this study triangulation is incorporated by using several sources of data and interviewing different stakeholders. Validity Validity (Construct, Internal and External) of this project refers to the ability of this study to scientifically answer the questions it is intended to answer (Blumberg et al., 2005). Construct validity refers to the extent to which operationalization of a construct does actually measure what the theory says it should measure (Bagozzi, 1991). Yin (2009) explains three methods to do so. First construct validity is enhanced by making sure of several sources of evidence. Secondly the chain of evidence used in this research is kept as clear as possible. Third point wise transcripts of the interviews are made, and send to the interviewees to comment on the interpretation of the researcher. After an approval the findings are suitable for the research. Internal validity is an inductive measure of the degree to which the outcomes of this study about causal relationships can be drawn, based on the following three points: 1) the measures used, 2) the research setting, 3) the whole research design. Good experimental techniques are experiments in which the effect of an independent variable on a dependent variable is studied under highly controlled conditions. Within this project, the research design, research setting and the measures used will be considered well in order to prevent a validity discussion. External validity concerns the extent to which the outcomes of this study can be held to be true for other cases. In other cases the people, time or place are different, but the outcomes must also be identical. In order to prevent the study from this discussion, the research conditions will clearly be elaborated. 25

26 Part 1 Literature Review 3. Theoretical background This chapter provides an overview of the theoretical background that has been deducted from the secondary sources. These secondary data sources are academic researchers in the area s related to the topic of this research. The information from these sources will be later on combined with the primary data to answer the main research question, in order to provide new insights for the scientific world. This chapter is build up as follows; first an elaboration of strategic consultancy firms is made. After this elaboration the topic of business models is addressed. The link with strategic consultancy firms is also explained. There-after the topic of business model/ model innovation is elaborated. As has been done before, this topic is linked with strategic consultancy firms too. Finally a short conclusion and discussion of the literature is provided Strategic Consultancy Strategic consultancy is a collective noun for the field of expertise of advisors that are focusing on projects with a strategic nature. Their customers hire a consultant if they don t have the knowledge their self s to achieve this result. For sake of this research ARCADIS, its subsidiaries (see Appendix II) and the competitors are regarded as a strategic consultancy firm because they provide their clients with strategic advice for environmental issues. The topics for these environmental advises are really broad, just as the clients; from SME s (Small Medium Enterprises) and local governments to MNE (Multi National Enterprises)/MNC (Multi National Clients and the EU (European Union). In (Appendix I) Table 7 an overview of the types of consulting services is presented. Another important characteristic of the consultancy market is the relationship building between client and consultant. A consensus driven relationship, which is open for affiliations and comments, allows consultants to develop the most suitable solution for their client. Finally it is important for consultants to build their network within and outside the firm. To provide their clients with new solutions building this network is essential. Without a good reputation the relational competence is hard to achieve. High reputation therefore can be deemed as a door opener and pre-condition for firms to award a project, (Kaiser and Ringlstetter, 2011). The reputation of the firm (branding the name), should be shown by using adequate references of successfully terminated projects. The back-office should document all these references well, to be able to provide them whenever needed. The new World of competition (Kash, 1989) has four underlying premises to be successful: 1) Aiming at hassle-free services is not possible; clients are demanding instantaneous, flawless en effortless services. 2) Good basic services are not good enough. Clients demand premium services, and these clients change their standard continually. 3) Companies can no longer compromise on quality and or product capabilities. Moreover a superior combination of both is needed. 4) Raising prices is not possible. Reduction of costs and working more billable are essential in order to stay competitive. In the world of strategic consultants the competition is high. Small firms with only one or a few employees are delivering services for prices far 26

27 below the market price. These called self-employed consultants (in Dutch: ZZP s (zelfstandige zonder personeel)), or SME s are providing services that are valuable for their money. But they cannot reach the high quality standard of the well-respected larger consultancy firms. The so called pricing paradox (Owusu-Manu et al., 2012) is of less of concern of these consultants in contract to the consultants of the larger MNE/MNC. Furthermore the job tile consultant is in contrast to many other job titles (such as lawyer, engineer, etc.) not a legally protected occupational title. Since there is no standardized training and or discipline-specific academic degree is required. This results in the fact that everybody may call their self consultant. This makes it easier for a person to start his own consultancy firm. Strictly translated the term consultant explained as specialist who gives expert advice or information. The bigger and more respected strategy consultancies (Booze, PWC and Deloitte for e.g.) recruit graduates, who do not have an economic background, but come with the necessary expertise (e.g. physicians, engineers or theologians). Nonetheless it is essential to have some intellectual abilities, such as analytical skills and problem solving competence. Furthermore some other characteristics like objectivity, discretion, willingness to learn, flexibility and the ability to cope with pressure and behavior, like e.g. communication skills are necessary. In Figure 3 the field (red cycle) in which the advisory S&B is mainly operating is graphically depicted. This cycle is known as the Policy Cycle. The baseline for this cycle is the Plan, Do, Check, Act model of Deming (1986), who is regarded as an expert on the topic of quality management. This cycle is translated into the Policy Cycle. The clients of firms such as ARCADIS Netherlands (and advisory S&B) can be roughly divided into three main categories: governmental, semi-governmental and public Business Models As the term business model intuitively suggests it has something with both with business and with models. Osterwalder et al., (2005) explains this as follows: Evaluatie Uitvoering Beleidsontwikkeling Implementatie (planvorming) Figure 3 Policy Cycle Business is the activity of buying and selling goods and services, or a particular company that does this, or work you do to earn money, pg (14); A Model is a representation of something, either as a physical object which is usually smaller than the real object, or as a simple description of the object which might be used in calculations, pg (14). PSF firms often offer several services, and thus the usage of multiple business models within a single firm would be beneficial. These business models can differ within a firms division or department. These findings are supported by den Hertog et al., (2010), who state that service firms can have different business models in their portfolio and that these firms may combine various new business models in one strategy. Business models are a trending topic in research. Good and sometime innovative business model(s) are essential for firms to survive in the current environment. The IBM CEO study 27

28 (2006) showed that business model innovation has a higher correlation with operating margin growth than any other type of innovation. This is in line with Osterwalder et al., (2005), who states that focusing on product innovations is not enough anymore. Osterwalder et al., (2005) presents a few reasons why business models fail. Understanding these risks help managers manage risks better. In his blog on he broadly categorized business model failures into four main reasons: 1) solving an irrelevant customer job, 2) flawed business model, 3) external threats, and 4) poor execution. Researchers are using business model and strategy interchangeably while others use them as two different concepts. Before the elaboration of the business model itself, a clarification of both concepts is needed. Despite all the literature and words spoken, business models are still relatively poorly understood (Linder and Cantrell, 2000). Firms have to develop a more sustainable competitive position and a strategy in order to adapt to the changing environment (Vanhaverbeke, 2003). The competition is increasing, and new entrants are entering the market with new and innovative business models (Vanhaverbeke, 2003). These new business models are sometimes disruptive for the market, and thus established firms have to adapt their current models. Firms innovating their business models have two choices in their strategy according to Chan Kim and Mauborgne (2000), [7]. (Business) Strategy refers to the choices made by the firm in respect to what, how and where they will do business. The business model then, elaborates on an architectural level rather than on a visionary level, the implementation and operationalizing of this strategy (Osterwalder et al., 2005). Teece (2010) even states that a business model is more generic. According to Magretta (2002) there is a practical difference between a strategy and a business model. A business model explains how the different (puzzle) parts fit to each other. In contrast to the strategy, that also describes how this enhances the competiveness of the firms with its product or service in the market. The business model is a blue print that allows designing and realizing the business structure and systems that constitute too the operational process and physical form of the company. This relationship (the Business Triangle (Figure 4) Osterwalder et al., (2005)) between strategy, the technology and the business organization are constantly subject to external pressures, like competitive forces, social change, technological change, customer opinion and legal environment. The definition of business models is explained in different ways. Osterwalder et al., (2005) describes the business model's Figure 4 Business Triangle, (Osterwalder et al., 2005) place in the firm as the blueprint of how a company does business. It is the translation of strategic issues, such as strategic positioning and strategic goals into a conceptual model that explicitly states how the business functions. The business model serves as a building plan that allows designing and realizing the business structure and systems that constitute the company s operational and physical form. Further some well-known explanations are: 1) the architecture for products, services and information flows, including a description of various business actors and their roles, the potential benefits for the various business actors, and the 28

29 sources of revenues (Timmers, 1998). 2) A statement of how a firm will make money and sustain its profit stream over time (Steward and Zhao, 2000). 3) A summation of the core business decisions and trade-offs employed by a company to earn profit (Hamermesh et al., 2002). 4) The more recent research of Osterwalder and Pigneur (2010) described the business model as the rationale of how an organization creates, delivers, and captures value. This last definition is very similar with the business model definition of Timmers (1998). Amit and Zott (2010) describe it as the bundle of activities that are conducted to satisfy the perceived needs of the market, including the specification of the parties that conduct these activities, and how these activities are linked to each other. These mentioned explanations are just a few of the many definitions of business models. In Appendix III a recent overview of the used definitions is presented. As can be deducted from this overview, there is not a single accepted definition of the business model. Nor is there a consensus on the components or attributes of which a business model is build up. This difference of views is caused by the abstraction level the researchers are evaluating this concept. From a more generic level (Magretta 2002) to a more concrete level (Timmers, 1998 and Osterwalder et al. 2005). A further discussion about the appropriate definition is out of scope of this research. According to Chesbrough (2007) a business model performs two important functions: value creation and value capture. There are several ways to look at business models. In general business models are examined on the firm-level, but Chesbrough and Rosenbloom (2002) are suggesting that a firm can have several distinctive business models. The theory of Osterwalder and Pigneur (2010) in combination with the theory of Chesbrough (2007) will be used during this project Business Model Framework There are many definitions of a business model, nevertheless in essence all these definitions share the same baseline. A business model consists of different building blocks (or components) that are beneficial to each-other. These blocks elaborate the way a firm executes and governs its business processes, creates the value proposition for a service Figure 5 Business model blocks linkage. for a group of specific customers, and thus yields a profit in the end. Osterwalder and Pigneur (2010) elaborated the definition of a business model with use of their business model canvas (see Appendix IV, Figure 11). This model consist of the following nine building blocks: value proposition, customer segments, distribution channel, customer relationships, revenue streams, key resources: key activities, key partners, and cost structure. In Figure 5 the link between the individual blocks is depicted. Figure 5 shows that the 9 building blocks are grouped into 4 sets. These sets are: 1) activity perspective (or 29